Restaking derivatives 2026 market overview

The restaking sector has matured into a significant pillar of the decentralized finance landscape, driven by the demand for capital efficiency and yield generation. By late February 2026, the broader restaking ecosystem held approximately $13.45 billion in total value locked (TVL), according to data from DAIC Capital. This substantial capital deployment underscores the high-stakes nature of these instruments, as users seek to maximize returns on their staked assets across multiple layers of the Ethereum and Solana ecosystems.

Restaking fundamentally allows validators to redeploy their staked cryptocurrency across other proof-of-stake (PoS) based services, creating a new class of financial derivatives. This mechanism enables the same underlying security to be shared among various networks, such as oracle providers, data availability layers, and bridge protocols. The result is a complex web of interdependent yields and risks, where the performance of one protocol can directly impact the returns and security posture of others.

To understand the current market dynamics, it is essential to look at the price action of the underlying asset. Ethereum remains the primary collateral for these restaking derivatives, and its valuation directly influences the attractiveness of yield-bearing tokens. The following chart illustrates the recent price movement of ETH, providing context for the yield opportunities available in the market.

The interplay between ETH's price performance and the yield generated by restaking protocols creates a unique risk-reward profile. While the $527,000 in daily yield generation reported by DAIC Capital highlights the income potential, it also reflects the sensitivity of these returns to market volatility. As the sector continues to evolve, investors must carefully plan around the trade-offs between yield optimization and the inherent complexities of shared security models.

EigenLayer Yield Optimization Mechanics

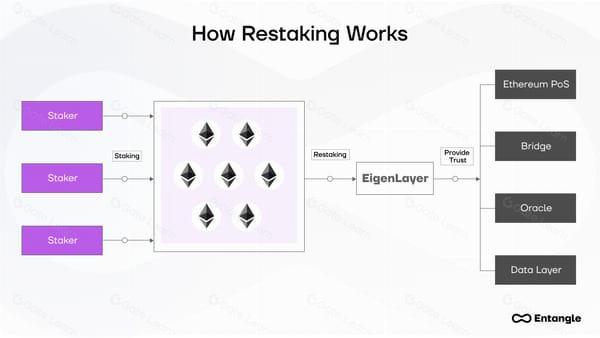

EigenLayer operates as a middleware layer that transforms Ethereum’s native Proof-of-Stake consensus into a shared security resource. By allowing stakers to restake their liquid staking tokens (LSTs), the protocol enables these assets to secure additional networks known as Actively Validated Services (AVS). This mechanism decouples security from the base layer, creating a marketplace where capital efficiency is maximized through cryptographic guarantees rather than isolated validator sets.

The core innovation lies in the reusability of staked ETH. When a user stakes ETH directly, the security is bound exclusively to Ethereum’s execution and consensus layers. Restaking introduces a second layer of obligation: the same staked assets must now also validate the integrity of external AVS protocols. This creates a compounding yield structure, where validators earn returns from Ethereum block rewards, transaction fees, and additional AVS-specific incentives simultaneously.

This architecture introduces a critical technical distinction between native staking and restaking. Native staking secures a single, highly battle-tested network with established slashing conditions. Restaking, however, requires the staker to assume the risk of multiple, often newer, protocols. If an AVS fails or is compromised, the shared security model means the underlying staked ETH can be slashed to compensate for the loss. This creates a high-stakes environment where yield is directly correlated to the security maturity of the AVS being supported.

The yield optimization potential is significant, but it is not risk-free. The protocol relies on a complex web of smart contracts and cryptographic proofs to ensure that validators cannot double-sign or act maliciously across different chains. For institutional participants, this means that yield is no longer a passive return on capital but an active management of counterparty and technical risk across a distributed ecosystem of secured services.

How EtherFi liquid restaking tokens work

EtherFi introduced the concept of liquid restaking tokens (LRTs) to solve the liquidity trap inherent in native restaking. When users restake ETH directly on EigenLayer, their capital is locked and earns yield, but it becomes inactive within the broader DeFi ecosystem. EtherFi’s approach allows users to receive a token—such as ezETH—that represents their restaked position. This token accrues restaking rewards while remaining a transferable asset that can be used as collateral in lending markets or automated yield strategies.

The core mechanism relies on EtherFi’s EigenLayer Restaking Vault. When a user deposits ETH, it is staked on EigenLayer to secure additional services. In return, the user receives ezETH, which tracks the value of the underlying staked ETH plus accumulated rewards. This design effectively unlocks the utility of restaked capital. Instead of sitting idle, ezETH can be deployed in liquidity pools or used to borrow against, creating a layer of composability that native restaking lacks.

This liquidity layer introduces complexity. Users must trust EtherFi’s smart contracts and the underlying EigenLayer infrastructure. If the restaking protocol experiences a slashing event, the value of ezETH can drop relative to the underlying asset. Also, the yield from ezETH is variable, depending on the performance of the services secured by the restaked ETH. Investors should view ezETH not just as a yield vehicle, but as a leveraged position on the broader Ethereum ecosystem’s security.

EigenLayer vs. EtherFi: A Direct Strategy Comparison

Choosing between EigenLayer and EtherFi requires understanding that they serve different points in the restaking value chain. EigenLayer acts as the foundational security layer, enabling native restaking of staked ETH to secure additional protocols. EtherFi operates primarily as a Liquid Restaking Token (LRT) protocol, aggregating user deposits to provide liquid exposure and automated yield optimization across multiple restaking strategies.

The core distinction lies in control versus convenience. EigenLayer is best suited for sophisticated operators who want direct exposure to slashing risks and specific actuator rewards. EtherFi appeals to users seeking passive income through automated management, where the protocol handles the complexity of distributing rewards from various restaked assets.

Both platforms are critical components of the current $13.45 billion restaking ecosystem, but their risk profiles diverge significantly. EigenLayer carries direct smart contract and slashing risk, while EtherFi introduces additional layers of abstraction and potential liquidity pool risks.

| Feature | EigenLayer | EtherFi | Primary Risk |

|---|---|---|---|

| Role | Security Layer | Liquid Restaking Token (LRT) | Smart Contract |

| Yield Source | Direct Actuator Rewards | Aggregated LRT Yields | Smart Contract |

| Liquidity | None (Native ETH) | Liquid (eETH) | Depegging |

| Complexity | High (Manual Setup) | Low (One-Click) | Operational |

| Slashing Exposure | Direct | Indirect/Shared | Slashing |

Decentralized Restaking Risks and Slashing

Restaking introduces a multiplier effect to risk. While it amplifies yield, it also exposes your staked assets to multiple layers of potential failure. Unlike standard staking, where a validator is penalized for a single chain’s rules, restaking protocols like EigenLayer and EtherFi require validators to meet the security requirements of several Actively Validated Services (AVSs) simultaneously.

The most severe risk is slashing. If a restaked validator acts maliciously or goes offline on any of the connected services, they can be slashed across all linked protocols. This means a single technical error or malicious act can result in the loss of the entire principal stake, not just a portion of it. The complexity of managing multiple security commitments increases the likelihood of human or code error.

Smart contract vulnerabilities add another layer of uncertainty. Restaking relies on complex code to manage the delegation of security and the distribution of rewards. A bug in the EigenLayer or EtherFi contracts could lead to the loss of user funds. As the ecosystem grows, the attack surface for exploiters expands. Users must trust that these protocols have undergone rigorous auditing and that their insurance mechanisms are sufficient to cover potential losses.

Finally, yield correlation poses a hidden risk. During market stress, the yields from different AVSs often correlate highly. This reduces the diversification benefits that restaking is often marketed to provide. In a severe downturn, the combined yield may drop to zero while the slashing risk remains high, leaving investors with significant downside exposure and minimal buffer.

Frequently asked questions about restaking

Is ETH expected to break $3,000 this year?

Reaching a $3,000 price point requires roughly a 30% increase from current levels, a move that remains plausible given Ethereum's recent momentum. Sustained institutional demand, evidenced by nine consecutive days of positive ETF inflows, provides the necessary liquidity support for such a breakout.

Can you still mine Ethereum in 2026?

Proof-of-work mining for Ethereum ended permanently with the Merge in 2022. Investors seeking yield must now turn to staking or restaking derivatives, which offer a more capital-efficient and energy-conserving alternative to traditional mining operations.

How does restaking impact broader ETH price action?

Restaking protocols like EigenLayer and EtherFi lock up significant amounts of ETH to secure additional networks. This reduced circulating supply creates upward pressure on price, while the yield generated from these derivatives provides an additional incentive for long-term holding rather than immediate sale.

No comments yet. Be the first to share your thoughts!