How restaking derivatives work in 2026

Liquid restaking tokens (LRTs) represent a shift from passive holding to active capital deployment. While standard liquid staking derivatives (LSDs) like stETH simply lock ETH to secure the Ethereum network and issue a receipt token, LRTs take that receipt token and restake it into additional protocols. This creates a layered security model where the same underlying capital helps secure multiple services, such as oracle networks or bridge infrastructure.

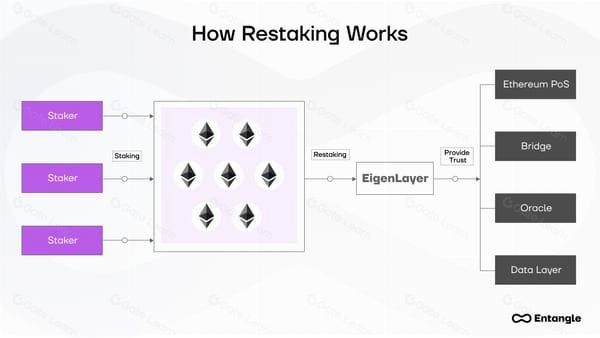

Think of standard staking as renting out your house to one reliable tenant who pays monthly rent. Restaking is like taking that tenant’s lease and subleasing portions of the property to other businesses, collecting additional fees while the original tenant remains in place. In 2026, this mechanism allows users to earn yield from Ethereum consensus rewards plus additional incentives from the restaked protocols.

The primary difference lies in capital efficiency and risk exposure. With LSDs, your capital is single-layered: it secures Ethereum and earns Ethereum rewards. With LRTs, your capital is multi-layered. You might restake into EigenLayer or similar activeset protocols to earn points, fees, or additional token emissions. This boosts potential returns but introduces new variables.

Understanding this mechanism is essential before comparing yields. An LRT’s APY is not just a single number from one protocol; it is a composite of base Ethereum staking rewards plus variable incentives from the restaking layer. As the ecosystem matures in 2026, these incentives become more complex, with some protocols offering real yield from usage fees and others relying on token emissions. This complexity is what separates simple staking from the more nuanced world of restaking derivatives.

Top liquid restaking tokens compared

Liquid restaking tokens (LRTs) have evolved from experimental yield instruments into core infrastructure for Ethereum's decentralized security layer. In 2026, the market is dominated by three protocols that handle the complexity of restaking while providing liquid derivatives: Ether.fi, Renzo, and Kelp DAO. Each protocol offers a distinct approach to custody, yield generation, and ecosystem integration, allowing validators and stakers to choose based on their risk tolerance and capital efficiency needs.

The primary value proposition of any LRT is the ability to earn Ethereum staking rewards plus additional restaking yields without locking up capital. However, the mechanisms differ. Ether.fi relies on a native node operator network, Renzo focuses on automated strategy allocation, and Kelp DAO emphasizes modular security and cross-chain compatibility. Understanding these structural differences is essential for evaluating yield sustainability and smart contract risk.

Comparison of Leading LRT Protocols

The following table breaks down the core operational differences between the top three liquid restaking tokens. This comparison highlights custody models, primary yield sources, and key ecosystem integrations to help you identify which protocol aligns with your strategy.

| Protocol | Custody Model | Primary Yield Source | Key Ecosystem Integration |

|---|---|---|---|

| Ether.fi | Node Operator Network | ETH Staking + Restaking | Native DeFi Integration |

| Renzo | Automated Allocation | ETH Staking + Strategy Yield | Cross-Chain Liquidity |

| Kelp DAO | Modular Security | ETH Staking + RSETH Yield | Multi-Chain Expansion |

Ether.fi stands out for its deep integration with the native Ethereum DeFi ecosystem. By allowing users to select specific node operators, it offers greater transparency and control over the security layer. This model appeals to validators who prioritize direct oversight of their staked assets and want to maximize yield through curated restaking strategies.

Renzo differentiates itself through automation. The protocol allocates staked assets across a diverse set of restaking strategies without requiring user intervention. This approach is ideal for passive investors who seek to capture yield from various restaking points of failure while minimizing the complexity of managing multiple positions.

Kelp DAO focuses on modularity, offering RSETH as a liquid restaking token that can be used across multiple chains. This flexibility allows users to deploy their restaked assets in various DeFi applications beyond Ethereum, potentially unlocking higher yields through cross-chain lending and borrowing markets.

Where the Yield Comes From

Restaking derivatives generate yield through two distinct layers: the base security of the network and the added utility of decentralized services. When you stake ETH directly, you earn the protocol's native reward for validating transactions. This is the floor. Restaking takes that same staked ETH and reuses it to secure additional networks, such as oracle systems, bridge validators, or zero-knowledge proof verifiers. The extra rewards from these secondary services are distributed to you, effectively stacking income streams on a single asset.

This dual-layer approach is what makes liquid restaking tokens (LRTs) fundamentally different from traditional staking. You are not just paying for security; you are renting out your validator's computational power to a broader ecosystem. As the restaking sector expands in 2026, the variety of services requiring validation grows, creating new opportunities for yield that did not exist in solo staking models. The yield is not magical; it is a direct payment for the additional security work your capital performs.

Capital Efficiency Explained

The primary advantage of LRTs over solo staking is capital efficiency. When you stake ETH directly, your capital is locked and illiquid. You cannot use it for other financial activities without unstaking, which often involves a waiting period and potential slashing risk. LRTs solve this by issuing a liquid token that represents your staked position. You can hold this token, trade it, or use it as collateral in other decentralized finance (DeFi) protocols while still earning the underlying staking rewards.

Think of solo staking as putting your money in a fixed-term certificate of deposit where you cannot touch it. LRTs are more like a money market account that pays interest but also allows you to withdraw or pledge the funds elsewhere. This liquidity premium is valuable. It allows you to hedge your position, provide liquidity to decentralized exchanges, or borrow against your stake without losing the yield-generating benefits of the restaking protocol. This flexibility is why LRTs have become a cornerstone of modern DeFi strategies.

EigenLayer Risks and Regulatory Scrutiny

Restaking amplifies yield potential by multiplying the utility of staked assets, but it simultaneously multiplies the attack surface. When you restake ETH through EigenLayer, you are not just securing the Ethereum network; you are providing cryptographic security to a growing ecosystem of Actively Validated Services (AVSs). This creates a complex web of dependencies where the failure of one protocol can cascade into others.

Slashing and Smart Contract Exposure

The core mechanic of restaking is shared security, which means shared risk. If an AVS operator misbehaves—such as by signing invalid transactions or going offline—they can trigger a slashing event that penalizes the restaked ETH. Because your assets are often routed through Liquid Restaking Tokens (LRTs) and their underlying smart contracts, you are exposed to two layers of code risk: the EigenLayer core contracts and the specific LRT protocol managing your position.

This "slashing risk" is the primary downside of the strategy. Unlike traditional staking, where penalties are limited to the validator set, restaking exposes your capital to the operational security of third-party services. A bug in an LRT wrapper or a malicious act by an AVS operator can result in immediate loss of funds, a risk that does not exist in single-layer staking.

The Evolving Regulatory Landscape

Regulators are increasingly viewing LRTs through the lens of traditional securities laws. Because LRTs represent a share in a pooled security product that generates yield from multiple sources, they may be classified as investment contracts. This classification introduces significant compliance hurdles for issuers and potential legal risks for users.

Legal analyses from firms like Katten Muchin Rosenman highlight that the SEC could scrutinize LRT providers for operating as unregistered securities exchanges or investment companies. As the restaking ecosystem matures, regulatory clarity will likely shift from ambiguity to enforcement, potentially restricting how LRTs can be marketed or traded in certain jurisdictions. Investors must monitor these developments closely, as regulatory action could impact the liquidity and legality of holding these derivatives.

Market performance and technical outlook

Restaking derivatives track Ethereum closely, but their yield mechanics create distinct risk profiles. The LRT market trend often amplifies ETH price movements while layering protocol-specific variables. Understanding this correlation helps separate structural yield from speculative beta.

The relationship between ETH and major LRTs like ETHFI or ezETH is visible on technical charts. When ETH consolidates, LRTs may show relative strength due to accumulated restaking rewards. However, during volatility spikes, these tokens often face higher liquidity friction than the base asset.

Technical analysis of LRT pairs requires monitoring both the ETH baseline and the specific LRT's trading volume. Breakouts in LRT price action frequently precede broader market shifts, acting as leading indicators for restaking demand. Traders should watch for divergence between price and volume as a signal of weakening momentum.

The underlying asset remains the primary driver. Restaking derivatives are essentially leveraged exposure to Ethereum's security model. When ETH trends upward, LRTs often outperform due to compounded yield. When ETH corrects, the yield cushion is rarely enough to offset capital depreciation, making risk management essential.

Frequently asked questions about LRTs

Liquid restaking derivatives (LRTs) are complex financial instruments that layer yield generation on top of Ethereum staking. Because they introduce smart contract risk and slashing exposure, understanding the mechanics is essential before allocating capital.

No comments yet. Be the first to share your thoughts!