How restaking derivatives changed yield

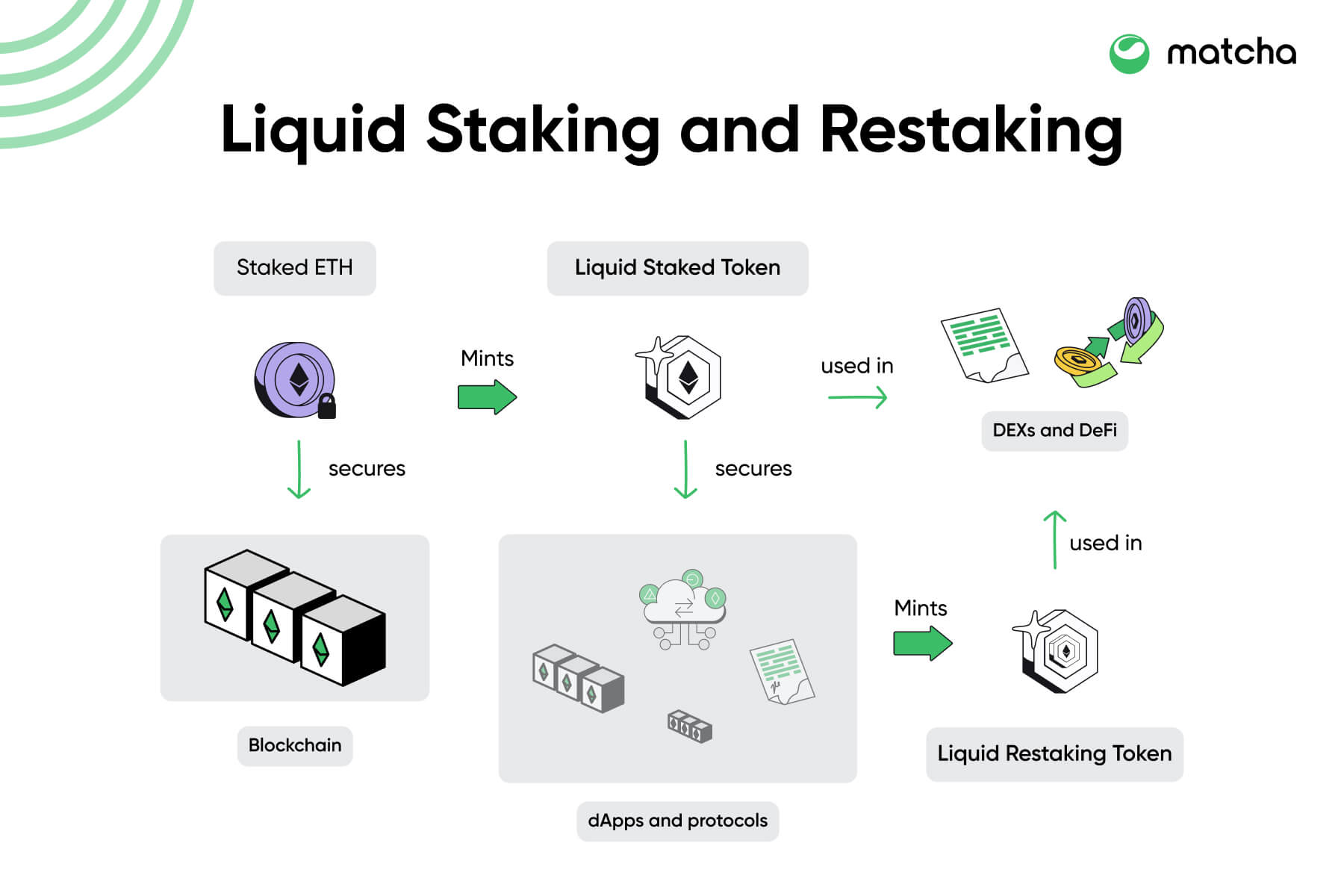

Traditional staking locks capital to secure a network, offering yield but freezing liquidity. Restaking derivatives, primarily Liquid Restaking Tokens (LRTs), decouple these functions. By allowing staked assets to provide security to multiple protocols simultaneously, LRTs unlock capital efficiency that simple staking cannot match. This shift transforms idle staking rewards into a multi-layered yield engine.

The mechanism is straightforward but introduces new complexity. An LRT represents staked ETH that continues to earn base consensus rewards while being deployed as collateral for other services, such as oracle networks or zero-knowledge rollups. This dual-use model amplifies returns, but it also layers risk. A failure in any downstream protocol can impact the underlying staked asset, creating correlation risks that were absent in single-layer staking.

In 2026, the landscape has matured beyond experimental protocols. Major LRTs now offer transparent risk frameworks and real-time monitoring of their restaked exposure. Investors no longer need to choose between yield and liquidity; they can hold LRTs to access both, provided they understand the underlying security assumptions. The key is evaluating which protocols the LRT supports and how those protocols are audited and monitored.

This evolution has made restaking a core component of DeFi portfolios. However, the yield advantage comes with a trade-off: increased complexity and potential smart contract exposure. Understanding these dynamics is essential for anyone considering LRTs as a primary yield strategy.

Top liquid restaking tokens ranked

The liquid restaking token (LRT) market in 2026 has shifted from speculative experimentation to a maturing infrastructure layer. Leading protocols like ether.fi, Renzo, and Puffer now compete on yield optimization, risk management, and cross-chain interoperability rather than just TVL growth. Choosing the right LRT requires understanding how each protocol structures its yield sources and manages the unique risks of restaking.

| Protocol | LRT Asset | Primary Yield Source | Key Risk Factor |

|---|---|---|---|

| ether.fi | ezETH | EigenLayer AVS + Ethereum Staking | Smart contract complexity & AVS downtime |

| Renzo | ezETH | EigenLayer AVS + Liquidity Vaults | Liquidity fragmentation across chains |

| Puffer | pufETH | EigenLayer AVS + Validator Diversification | Slashing risk from diversified validators |

| Karak | kETH | EigenLayer AVS + Modular Infrastructure | Newer protocol with limited historical data |

The table above highlights the structural differences between the top LRTs. While ether.fi and Renzo dominate in total value locked, Puffer’s approach to validator diversification offers a different risk profile. Karak, as a newer entrant, provides modular infrastructure but lacks the long-term track record of its predecessors.

Investors should note that LRT prices often trade at a discount or premium to their underlying staked ETH depending on market conditions and protocol performance. The live price widget above shows the current market value of Ethereum, which serves as the baseline for all LRT valuations. Always check the real-time exchange rate before swapping or staking, as these rates can fluctuate significantly during periods of high network congestion or AVS activity.

Where the yield comes from and where the risk hides

Liquid restaking tokens (LRTs) generate returns through a layered accumulation of value. The base layer is the native staking yield from Ethereum, currently hovering around 3-4%. The second layer comes from EigenLayer points, which represent potential future airdrops and protocol incentives for securing additional services. Some protocols also capture fees from restaked assets, though this is less consistent than the point incentives. For investors, this means the total yield is not just a single interest rate, but a composite of staking rewards, speculative points, and occasional protocol fees.

The risk profile is significantly more complex than simple ETH staking. Smart contract risk is amplified because LRTs involve multiple layers of code: the liquid staking protocol, the restaking layer, and the individual operator contracts. A vulnerability in any of these layers can lead to total loss of funds. Additionally, depegging risk exists because LRTs trade on open markets. If sentiment shifts or if a specific operator fails, the LRT price can drop below its backing value, creating a double loss for holders who sell at a discount.

TechnicalChart symbol="NASDAQ:ETH" chartStyle="candle" interval="1D" indicators='["volume","rsi"]' />

Comparing LRTs requires looking beyond the advertised APY. A high yield often signals higher risk exposure, such as reliance on volatile points or less battle-tested operators. Investors should scrutinize the specific operators backing their LRT and understand the slashing conditions for each service the protocol restakes into. The yield is not guaranteed; it is a compensation for taking on these compounded risks.

Regulatory scrutiny and compliance

The regulatory landscape for liquid restaking tokens (LRTs) has shifted from speculative ambiguity to active enforcement in 2026. Regulators are increasingly viewing LRTs not merely as yield-bearing derivatives but as unregistered securities or investment contracts. This classification stems from the centralized nature of many LRT protocols, where operators manage validator keys and reward distribution, creating a central point of control that triggers securities laws in jurisdictions like the United States.

The core concern for regulators is the separation of ownership and risk. When users deposit ETH to receive an LRT, they are often relying on a third-party operator to manage the underlying staking infrastructure. This dependency creates a fiduciary expectation that does not exist in pure decentralized protocols. Consequently, institutions face heightened compliance hurdles, as internal risk frameworks struggle to categorize assets that sit at the intersection of proof-of-stake consensus and traditional financial products.

Institutional adoption is now contingent on clear regulatory guardrails. Major financial players are delaying entry into LRT markets until they receive explicit guidance on custody, reporting, and liability. Without these frameworks, the risk of regulatory action against protocol operators remains a significant barrier to capital inflow. The current environment favors protocols that prioritize transparency and decentralized governance, as these structures are more likely to withstand regulatory scrutiny.

The emergence of regulated real-world asset (RWA) integrations in DeFi ecosystems offers a potential path forward. By anchoring LRT yields to compliant RWA structures, protocols may reduce their classification as speculative securities. However, this transition requires rigorous legal structuring and ongoing regulatory engagement. Until then, investors must navigate a fragmented global regulatory environment where compliance standards vary drastically by jurisdiction.

Frequently asked questions about restaking

How does restaking differ from standard liquid staking?

Standard liquid staking derivatives (LRTs) allow you to earn yield on staked ETH while maintaining liquidity. Restaking takes this a step further by reusing that same staked ETH to secure additional networks, such as Oracle or Bridge protocols. This layering improves capital efficiency but introduces complex interdependencies between the underlying validator set and the restaked services.

What are the primary risks of using LRTs in 2026?

The main risk is slashing cascades. If a validator is penalized for misbehavior, the loss can ripple through the restaking infrastructure, affecting multiple protocols simultaneously. Additionally, smart contract risk remains high; a vulnerability in an LRT bridge or orchestration layer could lead to total loss of the staked principal. The yield is not guaranteed and fluctuates with network demand for restaking services.

Is restaking yield sustainable long-term?

Current yields are driven by high demand for decentralized infrastructure services, but this is volatile. As more protocols adopt restaking, the supply of secured compute power increases, which may compress yields over time. Unlike traditional bond yields, restaking returns are directly tied to the speculative and utility demand for the specific services being secured by the restaked ETH.

No comments yet. Be the first to share your thoughts!