How restaking derivatives work in 2026

Restaking derivatives transform Ethereum into a shared security layer. When you stake ETH, you are not just earning yield; you are leasing out your validator’s security to other protocols. This mechanism allows a single asset to secure multiple networks simultaneously, creating a new tier of yield that sits on top of the base staking reward.

The mechanics are straightforward but powerful. Native staking yields, currently hovering between 2.8% and 3.2% for solo staking, compensate validators for maintaining the Ethereum mainnet. Restaking derivatives capture an additional "security premium." This premium is generated by securing secondary protocols via EigenLayer and similar networks. These protocols pay a fee to access Ethereum’s robust security guarantees, and that fee is passed back to the restaker.

This process creates a layered yield structure. The first layer is the consensus layer reward from Ethereum. The second layer is the AVS (Actively Validated Service) reward from the protocols you choose to support. Restaking derivatives, such as LRTs (Liquid Restaking Tokens), tokenize this combined exposure. They allow you to hold a liquid position that accrues both the base ETH yield and the additional security premiums without locking up your capital in multiple separate pools.

The efficiency of this system relies on the density of the security market. As more protocols seek Ethereum’s security, the demand for restaked ETH rises, potentially increasing the security premium. However, this also concentrates risk. If a secondary protocol secured by the restaked ETH fails or is exploited, the shared security model means the Ethereum validator’s stake could be slashed. This is the core trade-off: higher yields in exchange for exposure to the smart contract risks of the entire restaking ecosystem.

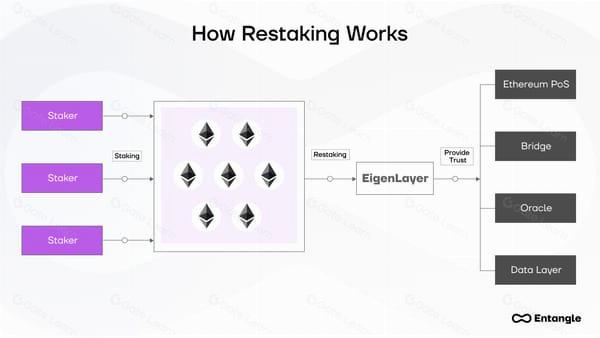

EigenLayer V2 and the shared security model

EigenLayer V2 marks a structural shift from a passive security layer to an active verification network. While the initial launch focused on restaking ETH to secure basic Ethereum infrastructure, V2 introduces Active Verification Services (AVS). This change expands the attack surface significantly, allowing Ethereum’s security budget to be rented out for more complex, high-value tasks.

In the original model, restakers provided proof-of-stake security but had limited direct interaction with the protocols they secured. V2 changes this by requiring restakers to actively validate specific services. These AVSs can range from oracle networks and data availability layers to cross-chain bridges. The result is a secondary market for security where Ethereum’s multi-billion dollar stake backs up external protocols.

This expansion creates new yield opportunities but also new risks. Restakers now face slashing conditions tied to the performance of these specific AVSs, not just Ethereum consensus. If an AVS validator fails to perform its duty, the restaker’s staked ETH can be penalized. This dynamic turns security into a tradable commodity, where yield is directly correlated to the reliability and demand of the verified service.

Top liquid restaking tokens compared

Liquid restaking tokens (LRTs) have evolved from simple yield wrappers into complex financial instruments. In 2026, the choice of LRT depends less on headline APY and more on the composition of that yield and the underlying risk profile. Major protocols like Ether.fi, Renzo, and Puffer manage this complexity differently, balancing native staking rewards with restaking points and liquidity incentives.

The following comparison highlights the structural differences between the leading LRT protocols. Understanding these distinctions is essential for selecting the right asset for your portfolio, as the risk factors vary significantly from protocol to protocol.

Protocol comparison

| Protocol | Primary Yield Source | Risk Factor | Liquidity Depth |

|---|---|---|---|

| Ether.fi (eETH) | Native ETH + EigenLayer Points | Smart Contract Risk | High |

| Renzo (ezETH) | Restaking Rewards + Points | Slashing Exposure | Medium |

| Puffer (pufETH) | Native Staking + Points | Insurance Pool Risk | High |

| KelpDAO (rsETH) | Restaking + LRT Incentives | Strategy Complexity | Medium |

This table illustrates the trade-offs inherent in liquid restaking. While Ether.fi offers deep liquidity and a simpler risk profile centered on smart contract security, Renzo and Puffer introduce additional layers of yield through restaking but also expose holders to slashing risks. The "Points" column refers to potential future airdrops or governance tokens, which currently represent a significant portion of the expected return for many LRT holders.

For investors, the decision often comes down to risk tolerance. Conservative holders may prefer Ether.fi for its established track record and high liquidity, which allows for easy entry and exit. More aggressive investors might explore Renzo or Puffer to capture higher yields from restaking rewards, accepting the additional complexity and potential slashing risks. Always verify the current yield composition, as incentives can change rapidly with market conditions.

Bitcoin restaking and cross-chain yield

Bitcoin restaking represents a structural shift in how dormant capital is utilized, moving beyond simple holding or liquid staking toward active security provision. Protocols like Babylon allow BTC holders to stake their assets to secure other Proof-of-Stake networks, introducing a new yield vector that decouples Bitcoin’s security from its own chain.

Unlike Ethereum restaking, which leverages staked ETH to provide additional security to the same ecosystem or parallel protocols, Bitcoin restaking creates a cross-chain trust model. The BTC remains locked in a Bitcoin-native wrapper or smart contract, but its hash power or staked value is attested to external chains. This allows Bitcoin to earn a "security premium" similar to the yield boost seen in EigenLayer, but without requiring the holder to bridge assets into an Ethereum Virtual Machine (EVM) environment where smart contract risk is higher.

The primary mechanism involves vaults that manage the staking process, ensuring that the BTC is not just locked but actively contributing to the consensus of a target chain. This creates a dual-yield structure: the base yield from the Bitcoin network (if any, though currently minimal for native PoW) and the additional yield from the external chain’s security fees. For holders, this transforms BTC from a static store of value into a productive asset with lower counterparty risk than traditional liquid staking derivatives, as the underlying asset remains on Bitcoin.

The expansion of this sector relies heavily on the maturity of cross-chain verification. As protocols like Babylon and others refine their attestation layers, the yield gap between Bitcoin staking and Ethereum staking may narrow, offering a more competitive risk-adjusted return for Bitcoin maximalists looking to engage with the broader DeFi ecosystem without abandoning Bitcoin’s security guarantees.

Managing slashing and systemic risk

Restaking derivatives introduce a unique layer of systemic risk that does not exist in standard staking. When you restake ETH to secure multiple Actively Validated Services (AVSs), you are not just providing yield; you are pooling security across distinct protocols. This creates a correlated risk environment where a failure in one AVS can trigger cascading penalties across the entire restaking portfolio.

Correlated slashing events

The primary danger in restaking is correlated slashing. If you delegate the same restaked ETH to several AVSs and one of them misbehaves—such as failing to provide valid attestations or signing invalid blocks—the validator node faces slashing penalties. Because your underlying ETH is shared across these services, the penalty applies to the entire stake, not just the portion explicitly allocated to the failing AVS. This means a single point of failure can wipe out yields and principal across all connected services.

Warning: Correlated slashing occurs when restaking the same ETH across multiple AVSs. A failure in one service can trigger penalties across your entire portfolio.

Smart contract vulnerabilities

Beyond validator behavior, the smart contracts governing restaking protocols are a significant attack vector. Liquid Restaking Tokens (LRTs) rely on complex code to manage the wrapping, unwrapping, and distribution of rewards. These contracts are often newer and less battle-tested than core Ethereum protocols. A vulnerability in the LRT contract or the underlying EigenLayer infrastructure could lead to exploits, frozen funds, or total loss of the restaked assets. The security of your restaked position is only as strong as the weakest link in this extended chain of contracts.

The role of decentralized insurance

Given these risks, decentralized insurance layers have become a critical component of safe restaking strategies. Protocols like Ether.fi and Renzo have integrated insurance funds or partnerships with decentralized insurance providers to cover potential slashing events or smart contract exploits. While these mechanisms do not eliminate risk entirely, they provide a financial safety net that can mitigate losses. Investors should prioritize restaking platforms that offer transparent insurance coverage and clearly define the conditions under which claims are paid.

No comments yet. Be the first to share your thoughts!