Restaking derivatives 2026 market overview

The restaking landscape has shifted from speculative expansion to institutional consolidation. Early 2025 enthusiasm, driven by the promise of infinite composability, collapsed under the weight of weak economics and excessive Active Validator Set (AVS) proliferation. Sub-1% incremental rewards failed to justify the operational complexity and security overhead for most participants, leading to a sharp contraction in total value locked (TVL) across unvetted protocols.

EigenLayer v2 has emerged as the primary architect of this new equilibrium. By introducing stricter operator requirements and more robust slashing mechanisms, the protocol has forced a hard fork between sustainable yield and speculative noise. This infrastructure upgrade has repositioned restaking from a high-beta trading narrative to a foundational layer for institutional-grade decentralized services. The focus has moved from asset quantity to asset quality, with capital flowing toward protocols that offer transparent, risk-adjusted returns.

Institutional players are now treating restaking derivatives not as yield farms, but as strategic balance sheet instruments. Corporate treasuries and regulated funds are adopting liquid restaking tokens (LRTs) only after rigorous due diligence on operator track records and smart contract audits. This institutional adoption is stabilizing the market, reducing volatility, and ensuring that yield generation is backed by real economic utility rather than token inflation.

The current market state is defined by this maturation. While retail participation has declined, the remaining capital is deeper and more committed. Restaking derivatives are now integral to Ethereum's security model, providing a reliable source of yield for long-term holders while supporting the development of decentralized infrastructure. The era of easy money is over; the era of sustainable, institutional-grade restaking has begun.

EigenLayer v2 mechanics and operator economics

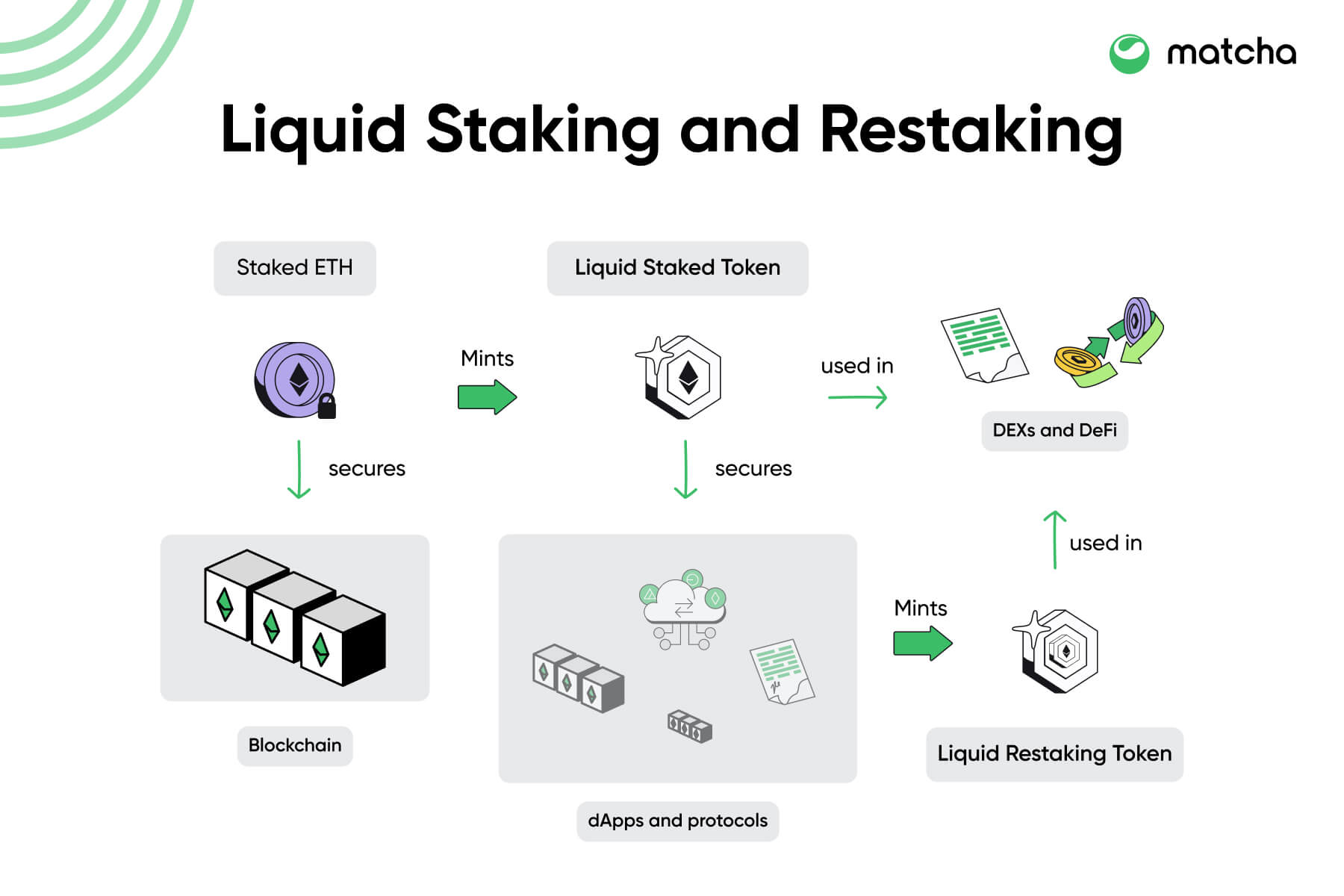

EigenLayer v2 represents a structural shift from the initial testnet phase to a production-grade infrastructure designed for institutional scalability. The core innovation lies in the introduction of granular risk management frameworks for Actively Validated Services (AVS). Unlike the monolithic security model of v1, v2 allows operators to opt into specific security profiles, enabling a more precise alignment between the risk exposure of the underlying staked assets and the yield generated by the service.

This architectural change directly impacts capital efficiency. Operators can now allocate their staked ETH to multiple AVSs with varying risk parameters, rather than committing to a single, broad security bundle. This modularity reduces the opportunity cost of staking, as capital is not locked into redundant security layers for services that do not require full Ethereum-level guarantees. The result is a more liquid and efficient market for decentralized security.

Slashing risks are mitigated through improved slashing condition verification and more transparent penalty structures. v2 introduces stricter validation requirements for operators, ensuring that those who manage high-value security bundles maintain the necessary technical infrastructure. This reduces the probability of catastrophic failures that could devalue the entire restaking ecosystem. The economic model now rewards consistent, high-quality performance rather than mere participation.

The economic incentives are recalibrated to favor long-term stability. Operators are incentivized to maintain high uptime and security standards, as penalties for misbehavior are more severe and immediate. This creates a more robust environment for LRT (Liquid Restaking Token) protocols, which can now offer more predictable yield products to their users.

Comparing Major Liquid Restaking Tokens

Liquid restaking tokens (LRTs) function as the primary interface for deploying capital into EigenLayer v2 and parallel restaking protocols. Unlike standard liquid staking tokens, LRTs layer additional yield opportunities atop base consensus rewards, introducing complex risk vectors that require rigorous institutional scrutiny. The 2026 market landscape is defined by divergent economic models: some protocols prioritize yield stability through conservative delegation, while others maximize returns via aggressive exposure to active validation services.

When evaluating leading LRTs, three metrics dominate the analysis: yield stability, underlying protocol support, and liquidity depth. Yield stability reflects the token’s ability to maintain consistent returns despite market volatility, often achieved through diversified slashing insurance or conservative smart contract architecture. Protocol support indicates the breadth of EigenLayer restaking slots and compatible L1/L2 networks the token can access, directly influencing its total value locked (TVL) capacity. Liquidity depth ensures that large institutional positions can be entered or exited without significant slippage, a critical factor for high-stakes capital deployment.

The following comparison highlights the structural differences between the dominant LRT protocols. These figures represent approximate annualized yields and risk profiles as of early 2026; actual returns fluctuate with network congestion and restaking demand.

| Protocol | Base Asset | Yield Profile | Primary Risk Factor |

|---|---|---|---|

| EigenLayer (eigenETH) | ETH | Moderate, Base + Restaking | Slashing exposure on AVSs |

| Ether.fi (ezETH) | ETH | High, Multi-Protocol | Smart contract complexity |

| Puffer Finance (pufETH) | ETH | Moderate-High, Insurance-Backed | Insurance fund solvency |

| Karak (kETH) | ETH | Moderate, Native Restaking | New protocol maturity |

Investors must contextualize these yield figures with their associated risk factors. Higher yields typically correlate with greater exposure to active validation services (AVSs) and complex smart contract layers, increasing the potential for slashing events or protocol failures. Institutional due diligence should prioritize protocols with transparent insurance mechanisms and audited codebases over those promising exceptional, unbacked returns.

Decentralized insurance mechanisms for restaking

Restaking exposes capital to novel failure modes, primarily slashable events and smart contract vulnerabilities. As EigenLayer v2 matures, the protocol shifts from a trust-based model to one requiring explicit risk pricing. Decentralized insurance protocols are evolving to cover these specific vectors, moving beyond generic DeFi coverage to address the unique economic mechanics of restaked assets.

The core challenge lies in the correlation of risk. Traditional insurance models rely on diversification, but restaking concentrates exposure across multiple Active Validation Services (AVS). A failure in a major AVS or the underlying EigenLayer contracts can trigger simultaneous claims, straining traditional capital pools. Insurers are now developing parametric triggers based on on-chain slash events and contract upgrade failures to automate payouts and reduce moral hazard.

Capital efficiency remains the primary driver for institutional adoption. Without adequate insurance, the cost of capital for restaking operations increases due to the risk premium demanded by operators and liquidity providers. Protocols that offer comprehensive coverage for both smart contract bugs and slashing events enable lower collateral requirements, making restaking viable for larger, risk-averse capital allocators.

The market is currently fragmented, with several specialized insurers emerging to cover restaking-specific risks. These protocols often require rigorous auditing of the underlying AVS contracts before providing coverage. Investors must carefully evaluate the solvency of the insurance provider and the clarity of the coverage terms, as regulatory uncertainty around these products remains high.

The integration of decentralized insurance with restaking protocols is still in its early stages. While the economic incentives are clear, the technical implementation of risk assessment and claim settlement requires further development. Investors should monitor the evolution of these insurance products as a key indicator of the long-term viability of restaking as a sustainable yield strategy.

Crypto yield farming trends 2026 outlook

The architecture of crypto yield farming has shifted from high-risk incentive programs to sustainable, protocol-level returns. In 2026, the market prioritizes economic durability over short-term token emissions. Investors are moving away from speculative farming toward strategies anchored in real yield generation and institutional-grade risk management.

Liquid restaking derivatives (LRTs) have become a central pillar of this transition. By allowing staked assets to secure multiple networks simultaneously, these derivatives offer diversified yield streams without requiring additional capital deployment. This efficiency addresses the capital fragmentation issues that plagued earlier DeFi cycles, creating a more robust yield infrastructure.

EigenLayer v2 is emerging as the technical standard for this new era. Its updated framework provides clearer economic security models and enhanced slashing conditions, reducing the systemic risk associated with restaking. This institutional-grade clarity is attracting capital that previously avoided DeFi due to regulatory and technical uncertainty.

While returns remain volatile, the underlying mechanics now favor long-term holding. The focus has moved from maximizing APY through leverage to minimizing risk through diversified, protocol-native yield. This shift marks a maturation of the market, where yield is a function of network utility rather than artificial incentives.

No comments yet. Be the first to share your thoughts!