What are restaking derivatives?

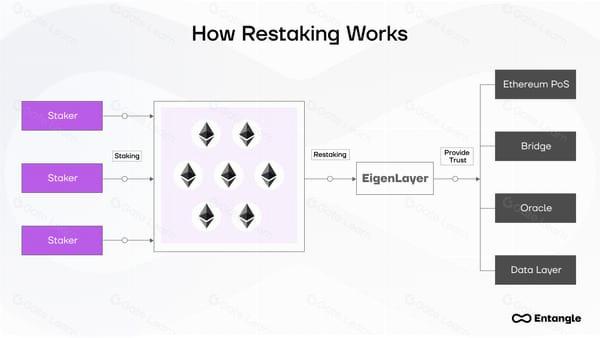

Restaking derivatives represent the next evolution of Ethereum staking, moving beyond passive yield generation into a complex ecosystem where security becomes a reusable resource. While basic liquid staking tokens (LSTs) like stETH or rETH simply tokenize staked ETH to maintain liquidity, restaking derivatives—often called Liquid Restaking Tokens (LRTs)—layer additional yield on top of that foundation. They do this by locking already-staked ETH into a second network, such as EigenLayer, to secure secondary protocols like oracle networks or bridge validators.

This mechanism allows a single unit of staked ETH to simultaneously secure the Ethereum mainnet and multiple restaked services. The result is a composite yield stream: the base Ethereum validator rewards plus additional incentives from the restaking layer. For 2026 DeFi strategies, this distinction is critical. It transforms staking from a static savings account into an active security market, but it also introduces significant smart contract complexity and correlated risk.

The primary appeal lies in the enhanced yield potential, which can significantly outperform traditional staking APYs. However, this comes with the trade-off of extended slashing risk. If a restaked service fails or is compromised, the underlying staked ETH can be penalized, affecting the value of the derivative. Understanding this layered structure is essential for any investor evaluating risk-adjusted returns in the current market.

EigenLayer and the LRT Protocol Landscape

EigenLayer has established itself as the central infrastructure layer for restaking, enabling Ethereum validators to secure additional networks through Actively Validated Services (AVSs). This mechanism allows capital to be reused across multiple protocols, creating a new class of derivatives known as Liquid Restaking Tokens (LRTs). In 2026, the market is defined by how these protocols manage the complexity of slashing risk and yield distribution while maintaining liquidity.

The primary LRT providers have evolved beyond simple wrappers to offer active yield optimization and risk mitigation. EigenLayer’s role is foundational; it does not issue LRTs itself but provides the shared security model that allows protocols like Ether.fi, Renzo, and Puffer to operate. These providers compete on their ability to diversify yield sources, including MEV rewards and AVS fees, while offering users a seamless exit path through their derivative tokens.

Understanding the distinctions between these protocols is critical for capital allocation. The following comparison highlights the core differences in yield generation, underlying asset support, and risk profiles across the leading LRT platforms.

| Protocol | Primary Yield Source | Asset Support | Risk Profile |

|---|---|---|---|

| Ether.fi | Staking + MEV + AVS fees | ETH, cbETH, rsETH | Moderate - Diversified AVS selection |

| Renzo | Restaking points + Auto-compounding | ezETH, ETH | Low-Moderate - Automated rebalancing |

| Puffer | Staking + Insurance pool | pufETH, ETH | Moderate - Slashing insurance model |

| Kelp DAO | RSETH yield + DeFi integration | rsETH, ETH | Low - Focus on liquid staking derivatives |

The choice of LRT often depends on the user’s tolerance for smart contract complexity and AVS-specific risks. While EigenLayer provides the security layer, the individual LRT protocols bear the responsibility of managing the underlying assets and distributing yields. Investors must evaluate not just the APY, but the robustness of the risk management frameworks each provider has implemented to protect against potential slashing events or protocol failures.

Where the Yield Comes From

Restaking derivatives layer multiple income streams on top of a single asset, creating a composite yield that exceeds native staking returns. The foundation is the base staking reward, which compensates validators for securing the Ethereum network. In 2026, this baseline remains the primary anchor for all LRT valuations, providing a floor for performance. Without this underlying security premium, the restaking layer has no foundation to build upon.

The second layer comes from restaking rewards. By restaking their liquid staking tokens (LSTs) on protocols like EigenLayer or EtherFi, users delegate their Ethereum security to additional services, such as oracles, RPC providers, or bridge operators. These services pay a premium for this security, which flows back to the LRT holders. This is where the yield delta originates. The more demand for decentralized infrastructure, the higher the restaking reward component becomes. This mechanism effectively monetizes the same capital for multiple distinct purposes simultaneously.

A third, more volatile source is Maximum Extractable Value (MEV). Restaking protocols often integrate MEV-boost or similar frameworks to capture value from transaction ordering. While base and restaking rewards are relatively predictable, MEV can fluctuate significantly based on network congestion and trading activity. For high-stakes investors, this variability introduces risk that must be weighed against the potential upside. The combination of these three sources—staking, restaking, and MEV—creates the total APY advertised by most LRTs.

Capital Efficiency Explained

The true innovation of LRTs is not just higher yield, but capital efficiency. Traditional staking locks assets for extended periods, reducing liquidity. LRTs solve this by issuing a derivative token that represents the staked asset. This token can be used in DeFi protocols for lending, borrowing, or liquidity provision while still earning staking rewards. This double-dip capability allows capital to work harder without sacrificing yield.

For example, an investor can stake ETH, receive an LRT, and then deposit that LRT into a lending market to borrow stablecoins. The borrowed funds can be reinvested, effectively leveraging the initial position. This circular flow amplifies returns but also increases exposure to liquidation risks and smart contract vulnerabilities. Understanding this leverage mechanism is essential for assessing the true risk profile of any LRT.

Smart contract and slashing risks

Restaking amplifies yield by locking already-staked assets into secondary networks, but it also concentrates risk in ways that simple staking does not. When you restake, your capital becomes collateral for multiple protocols simultaneously. This creates a complex web of dependencies where a failure in one layer can cascade into others. The primary vulnerabilities fall into two categories: smart contract bugs and slashing penalties on Actively Validated Services (AVSs).

Smart contract vulnerabilities

The code governing restaking protocols, such as EigenLayer, introduces additional attack surfaces compared to native staking. While the Ethereum base layer has been battle-tested for years, the middleware and AVS contracts are newer and less audited. A vulnerability in a restaking contract could lead to the loss of restaked ETH or LRT tokens. Unlike native staking, where your stake is only at risk for Ethereum consensus errors, restaking exposes your capital to the specific smart contract risks of every AVS you support.

Slashing conditions on AVSs

Slashing is the mechanism by which validators are penalized for misbehavior. In restaking, you can be slashed not just for Ethereum consensus errors, but also for failing to perform the duties required by an AVS. If an AVS requires you to sign off on transactions and you fail to do so, or if you act maliciously, your restaked assets can be penalized. This means your Ethereum stake is now at risk for the operational security of unrelated protocols. The complexity of managing these obligations increases the likelihood of human error or technical failure, leading to potential losses.

Restaking amplifies yield but also concentrates risk; slashing events on Actively Validated Services can impact restaked assets.

Mitigating exposure

To manage these risks, investors should carefully review the audit status and track record of each AVS before restaking. Diversifying across multiple AVSs can reduce the impact of a single failure, but it also increases the complexity of monitoring. Understanding the specific slashing conditions of each protocol is essential. The trade-off is clear: higher yields come with the responsibility of managing a broader set of technical and operational risks.

Choosing the right LRT strategy

Selecting a Liquid Restaking Token (LRT) requires matching your risk tolerance to your yield targets. The market is no longer a simple choice between holding ETH and staking it; it is a spectrum of leverage and exposure. Your decision should hinge on whether you prioritize capital preservation, yield maximization, or portfolio flexibility.

For investors seeking the lowest complexity, pure liquid staking tokens (LSTs) like rETH or stETH remain the foundation. These assets offer yield with minimal additional risk layers. They are ideal for those who want to earn staking rewards without exposing their principal to the smart contract risks inherent in restaking protocols. If your goal is simply to earn yield while maintaining the option to trade or use the asset as collateral on lending platforms, an LST is the most direct path.

If you are willing to accept higher risk for enhanced yield, LRTs that restake into protocols like EigenLayer or Kerberos become relevant. These strategies layer restaking rewards on top of base staking yields. However, this comes with increased smart contract exposure and potential slashing risks. This approach suits investors who understand the mechanics of restaking and are comfortable with the possibility of temporary lock-ups or reduced liquidity during market stress.

The final consideration is liquidity and composability. Some LRTs are more deeply integrated into DeFi ecosystems, allowing for easier borrowing or trading. Others may offer higher yields but suffer from lower trading volumes or higher slippage. Evaluate the token’s usage across DEXs and lending platforms. A strategy that offers high yield but cannot be easily deployed elsewhere may lock up your capital unnecessarily. Choose the LRT that balances yield with the liquidity you need for your broader financial plan.

Market outlook for restaking derivatives

The restaking market in 2026 has shifted from experimental yield farming to a core infrastructure layer for decentralized finance. Liquid restaking tokens (LRTs) now serve as the primary vehicle for capturing diversified yield across new L1s and L2s, moving beyond simple Ethereum staking rewards. This transition is driven by smart money seeking higher efficiency in capital deployment, as restaking allows validators to secure multiple networks simultaneously.

Regulatory clarity remains the defining variable for institutional adoption. While platforms like EigenLayer have pioneered the model, the lack of uniform global standards has created a cautious environment for traditional finance entrants. However, recent guidance from major financial authorities suggests a path toward compliance for tokenized derivatives, provided they meet strict custody and transparency requirements. This regulatory tailwind is beginning to unlock institutional capital that was previously sidelined by uncertainty.

Institutional adoption is accelerating, with major custodians and asset managers integrating restaking protocols into their broader DeFi strategies. The focus has moved from speculative yield chasing to sustainable, risk-adjusted returns backed by real-world utility. As the ecosystem matures, the distinction between traditional staking and restaking is blurring, with LRTs becoming a standard component of diversified crypto portfolios.

The trajectory points toward a more consolidated market where only protocols with robust security audits and transparent risk management will survive. Investors are increasingly prioritizing platforms that offer clear governance structures and insurance mechanisms against slashing events. This maturation is essential for the long-term viability of restaking as a pillar of the decentralized economy.

No comments yet. Be the first to share your thoughts!