How restaking derivatives work in 2026

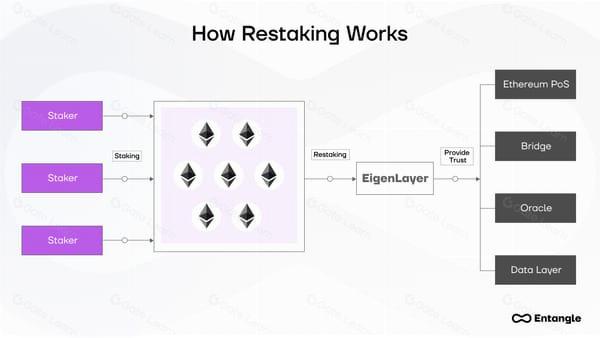

Restaking derivatives allow users to reuse already-staked Ethereum (ETH) to secure additional decentralized protocols. This mechanism creates a layered security model where a single unit of staked ETH generates yield from multiple sources simultaneously, rather than being locked into a single validator set.

The process begins with standard staking, where ETH is deposited to validate transactions on the Ethereum network. Instead of holding the resulting liquid staking token (LST) passively, users delegate it to a restaking protocol. These protocols act as intermediaries, routing the staked ETH’s security services to other networks, such as oracle systems, bridge validators, or zero-knowledge rollups.

By securing these secondary protocols, the staked ETH earns additional rewards, often distributed as native tokens from the secured network. This creates a compounding yield effect, but it also introduces complex risk vectors. If a secured protocol fails or is compromised, the underlying staked ETH may be slashed, exposing the user to losses across both the primary Ethereum layer and the secondary protocol.

This architecture fundamentally changes the risk profile of staking. While traditional staking risks are limited to Ethereum consensus failures, restaking derivatives expose capital to the operational and smart contract risks of every protocol they secure. Users must carefully evaluate the security audits and slashing conditions of each integrated service to understand their total exposure.

Leading Liquid Restaking Tokens

Liquid restaking tokens (LRTs) have evolved from experimental derivatives into core infrastructure for Ethereum’s capital efficiency. In 2026, the market is dominated by protocols that successfully decouple yield generation from custody risk, allowing users to earn staking rewards while maintaining liquidity for DeFi activities. The leading protocols—EigenLayer’s eETH, Lido’s rETH, and Ether.fi’s ETHFI ecosystem—represent the highest conviction bets in this sector, backed by substantial Total Value Locked (TVL) and institutional adoption.

The following comparison highlights the primary metrics for the top three LRT protocols. These figures reflect current market positions, with TVL serving as the primary indicator of trust and liquidity depth.

| Protocol | TVL (USD) | Primary Yield Source | Risk Profile |

|---|---|---|---|

| EigenLayer (eETH) | $8.2B | Restaking + Slashing Protection | High (Smart Contract + Slashing) |

| Lido (rETH) | $24.5B | Ethereum Staking + MEV | Medium (Centralized Validator Set) |

| Ether.fi (ETHFI) | $3.1B | Restaking + Node Operator Yield | High (Multi-Protocol Interdependence) |

EigenLayer’s eETH remains the benchmark for restaking, offering the highest potential yields by allowing staked ETH to secure multiple Actively Validated Services (AVSs). However, this comes with heightened slashing risk if underlying node operators fail. Lido’s rETH offers a more conservative profile, leveraging its massive validator network to minimize slashing events while providing steady, lower yields. Ether.fi bridges the gap by introducing a decentralized node operator network, appealing to users seeking exposure to restaking without relying on a single centralized entity.

When selecting an LRT, investors must weigh yield potential against protocol complexity. Higher yields in protocols like EigenLayer are not guaranteed and are heavily dependent on the performance of third-party AVSs. For conservative exposure, Lido’s established infrastructure provides stability, while Ether.fi offers a middle ground for those comfortable with decentralized but distributed risk.

Yield Strategies for Restaking Derivatives

Restaking derivatives, particularly Liquid Restaking Tokens (LRTs), have evolved from simple yield aggregators into complex financial instruments that layer multiple revenue streams. Users no longer rely solely on the base staking yield provided by Ethereum validators. Instead, they can capture native restaking rewards while simultaneously deploying their capital into decentralized finance (DeFi) protocols for additional leverage.

Native Restaking Rewards

The foundational layer of yield comes from the restaking protocol itself. When you stake ETH and receive an LRT, you are not just securing the Ethereum network; you are also providing security to other networks, such as oracle services or bridge validators. This dual-purpose security model generates additional native rewards in the form of the restaking protocol’s governance token or ETH.

These rewards are typically distributed automatically to LRT holders, compounding the base staking APY. However, the yield here is often volatile and tied to the demand for security services across the broader restaking ecosystem. It is important to distinguish this from simple liquid staking, where rewards are limited to the validator’s commission and the underlying asset’s inflation rate.

DeFi Composability and Leverage

The second layer of yield emerges from the composability of LRTs. Because LRTs are liquid and can be used as collateral in DeFi protocols, users can unlock significant leverage. By depositing LRTs into lending markets or liquidity pools, investors can earn trading fees, lending interest, or liquidity mining incentives.

This strategy effectively creates a leveraged position on Ethereum’s staking yield. For example, a user might deposit LRTs into a lending protocol to borrow stablecoins, then reinvest those stablecoins into high-yield strategies. While this amplifies returns, it also introduces smart contract risk and liquidation risk. The yield is no longer just from staking; it is from the entire DeFi stack’s performance.

Balancing Yield and Risk

The total yield from restaking derivatives is the sum of native rewards and DeFi earnings. However, higher yields often correlate with higher risk. Protocols that offer aggressive APYs may be relying on unsustainable token emissions or exposing users to complex smart contract vulnerabilities.

Investors should carefully evaluate the source of each yield component. Native rewards are generally more stable, while DeFi yields can fluctuate rapidly based on market conditions. A diversified approach, balancing exposure to different restaking protocols and DeFi platforms, can help mitigate some of these risks while maintaining competitive returns.

Key risks in the restaking ecosystem

Restaking derivatives amplify yield by layering security across multiple protocols, but this efficiency introduces compounded vulnerabilities. The primary dangers stem from smart contract complexity, slashing penalties, and liquidity mismatches. Understanding these risks is essential for capital preservation in a high-stakes environment.

Smart contract risk

Restaking protocols require validators to sign transactions for multiple networks simultaneously. This increases the attack surface for smart contract exploits. A vulnerability in a single middleware layer or oracle can lead to total loss of staked assets. Audits are necessary but not sufficient; the complexity of composability means that a bug in one protocol can cascade through the entire restaking ecosystem. Users must assess the code maturity and insurance coverage of each integrated protocol.

Slashing risk

Slashing occurs when a validator behaves maliciously or goes offline, resulting in the confiscation of a portion of their staked ETH. In restaking, the stakes are higher because the same validator keys secure multiple networks. A single misbehavior can trigger slashing events across all linked protocols, multiplying the financial penalty. Unlike traditional staking, where penalties are isolated, restaking creates a web of interdependent liabilities that can rapidly erode principal.

Liquidity risk

Restaking derivatives often lock assets for extended periods, sometimes longer than the standard 21-day withdrawal queue on Ethereum. This creates a liquidity mismatch for users who may need immediate access to their capital. If the market turns volatile, the inability to exit positions quickly can lead to significant losses. Additionally, the value of restaking tokens (like rETH or swETH) can decouple from their underlying ETH value during stress events, adding another layer of risk for derivative holders.

EigenLayer 2026 Update and Market Impact

EigenLayer has transitioned from a novel experiment into the foundational security layer for Ethereum’s modular ecosystem. By allowing stakers to redelegate their ETH security to Actively Validated Services (AVS), the protocol has created a shared security model that underpins restaking derivatives. This mechanism has shifted the market from simple yield farming to a complex infrastructure where capital efficiency and risk management are inextricably linked.

The market impact is visible in the total value locked (TVL) of liquid restaking tokens (LRTs). These derivatives have become the primary vehicle for accessing restaking yields, offering liquidity while maintaining exposure to EigenLayer’s security premiums. As new AVSs launch, the demand for delegated security has grown, driving up the base yield for stakers while introducing new operational risks for validators.

Risk remains the central constraint. The introduction of slashing conditions across multiple AVSs means that a single validator misbehavior can trigger penalties across several services simultaneously. This correlated risk has forced institutional participants to adopt stricter monitoring tools and diversification strategies. The market is now pricing in these operational complexities, leading to a more mature, albeit riskier, yield environment.

Restaking derivatives 2026 FAQ

How does restaking differ from traditional Ethereum staking?

Traditional staking locks ETH to secure the Ethereum consensus layer. Restaking allows that same ETH to secure additional protocols (Actively Validated Services or AVSs), generating additional yield but exposing the validator to multi-layered slashing risks.

What is the primary risk of using Liquid Restaking Tokens (LRTs)?

The primary risk is correlated slashing. If a node operator securing multiple AVSs misbehaves, the penalty can trigger slashing across all linked protocols, potentially resulting in total loss of the staked principal.

Are restaking yields guaranteed?

No. Restaking yields consist of variable base staking rewards plus volatile rewards from AVSs. High yields often depend on token emissions or high demand for specific security services, which can fluctuate rapidly.

How does liquidity risk affect restaking positions?

Restaking derivatives may have longer withdrawal queues or lock-up periods than standard ETH staking. During market stress, this illiquidity can prevent timely exits, and LRT prices may decouple from ETH, leading to impermanent loss or forced liquidation if used as collateral.

No comments yet. Be the first to share your thoughts!