Restaking derivatives 2026 market snapshot

The restaking derivatives market has matured into a significant infrastructure layer for Ethereum. By late February 2026, the broader sector recorded approximately $13.45 billion in total value locked (TVL) [[src-serp-3]]. This capital accumulation signals a shift from experimental yield farming to a structured financial market, where derivatives provide the liquidity and leverage necessary for institutional participation.

The value proposition of restaking derivatives extends beyond simple yield. While Ethereum solo staking offers a base yield of roughly 2.8% to 3.2%, restaking protocols layer a "security premium" on top of this foundation [[src-serp-7]]. This premium compensates validators for providing shared security to other networks or services, effectively monetizing the baseline consensus effort. Derivatives capture this spread, allowing users to trade exposure to security premiums without managing the underlying validator keys.

Market dynamics are closely tied to the broader health of the Ethereum ecosystem. The growth in TVL correlates with increased demand for decentralized compute and data availability, which rely on restaked Ethereum security. As these new use cases scale, the derivatives market provides the necessary price discovery mechanism, turning static staking rewards into tradable, leveraged instruments.

How liquid restaking tokens generate yield

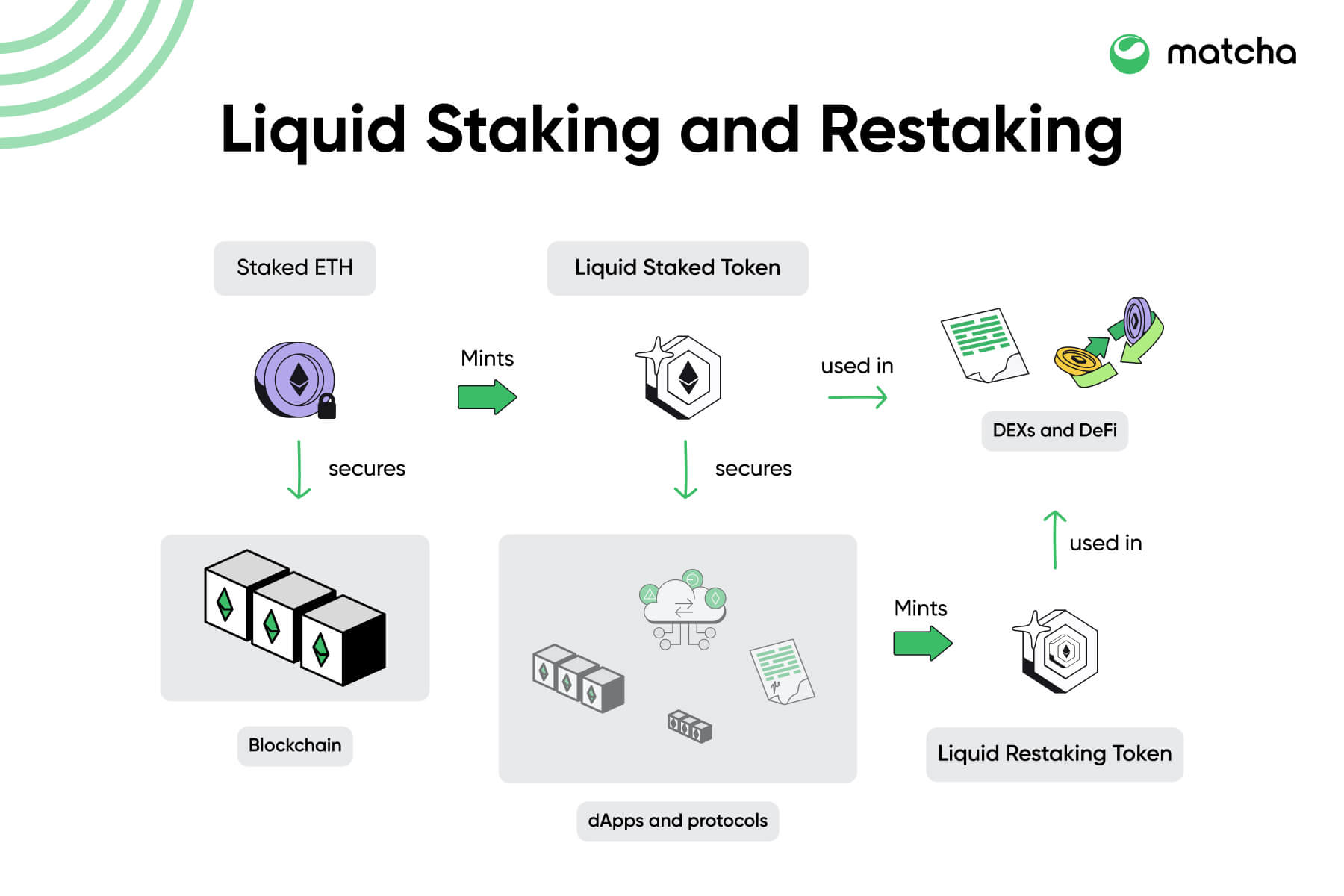

Liquid restaking tokens (LRTs) like ezETH or rsETH function as a yield multiplier. They take the base security of native staking and layer additional value on top through composability. The difference is mechanical: native staking pays you to secure one chain, while restaking pays you to secure multiple networks simultaneously.

When you stake ETH natively, you earn a base yield for validating the Ethereum network. Restaking protocols like EigenLayer allow you to redeploy that same staked ETH to secure "restaking services"—often referred to as Actively Validated Services (AVSs). These services might include oracle networks, bridge validators, or decentralized compute markets. By reusing the same cryptographic proof of stake, you earn a "security premium" for each additional service your stake backs.

This creates a compounding effect. You are not just earning interest; you are renting out your validator's security posture to other protocols. As of early 2026, this structure allows restakers to capture yields significantly above the 2.8% to 3.2% base rate of solo staking, provided the AVSs they support are active and paying out rewards.

EigenLayer vs. Babylon: ETH and BTC models

EigenLayer and Babylon represent the two dominant paths for restaking derivatives in 2026, each securing a different native asset with distinct risk profiles. EigenLayer extends Ethereum’s shared security to new protocols, while Babylon unlocks Bitcoin’s hash rate for similar purposes. Understanding their structural differences is essential for evaluating yield potential.

Ethereum’s Shared Security

EigenLayer allows stakers to restake their liquid staking tokens (LSTs) like stETH or wstETH to secure "Actively Validated Services" (AVS). This model creates a deep liquidity pool for Ethereum’s ecosystem, enabling new protocols to borrow security without bootstrapping their own validators. The yield comes from the underlying ETH staking rewards plus additional fees paid by the AVSs. However, this introduces complex slashing risks, where a validator’s entire restaked balance can be penalized if they fail to perform their duties for an AVS.

Bitcoin’s Native Staking

Babylon takes a different approach by introducing proof-of-stake security to Bitcoin without altering its consensus layer. It leverages Bitcoin’s existing hash rate, allowing BTC holders to stake their coins in time-locked contracts to secure other networks. Because Bitcoin’s security model is based on work rather than stake, Babylon’s slashing conditions are designed differently, often relying on economic penalties rather than validator slashing. This creates a unique yield opportunity that is decoupled from Ethereum’s validator set dynamics.

Side-by-Side Comparison

| Feature | EigenLayer | Babylon |

|---|---|---|

| Native Asset | Ethereum (ETH) | Bitcoin (BTC) |

| Security Model | Shared Security (AVS) | Time-Locked Staking |

| Primary Yield Source | ETH Staking + AVS Fees | BTC Staking Rewards |

| Slashing Risk | Validator-based | Economic/Contract-based |

| Liquidity | Liquid (via LSTs) | Locked (Time-locked) |

Key choices that change the plan

The choice between these models often comes down to liquidity preferences and asset exposure. EigenLayer offers higher liquidity since restaked assets remain in the form of LSTs, which can be traded or used in other DeFi strategies. Babylon typically requires locking BTC for specific periods, reducing liquidity but potentially offering higher yields due to the scarcity of staked Bitcoin. Investors must weigh the complexity of Ethereum’s slashing conditions against the lock-up periods of Babylon’s contracts.

| Asset | Protocol | Est. TVL | Risk Profile |

|---|---|---|---|

| ETH | EigenLayer | High | Slashing |

| BTC | Babylon | Medium | Lock-up |

Slashing risks and systemic exposure

Restaking derivatives amplify yield by recycling staked assets, but they also multiply risk. When you restake, your capital secures multiple services simultaneously. This creates a scenario where a single validator failure can trigger correlated slashing events across the entire restaking stack. Unlike isolated staking, where one fault affects one reward pool, restaking links your security deposit to the performance of all active modules. If a shared validator goes offline or acts maliciously, the protocol may slash your stake to compensate for the breach, reducing your principal regardless of which specific service was impacted.

The systemic exposure is further complicated by smart contract vulnerabilities. Restaking protocols like EigenLayer introduce new layers of code complexity. Each additional abstraction—whether it’s a liquid restaking token (LRT) wrapper or an intent-based solver—adds a potential attack surface. A bug in one of these intermediate contracts can lead to total loss of funds, even if the underlying Ethereum consensus layer remains secure. Investors must recognize that the yield is not just a reward for locking capital, but a premium for accepting this compounded technical risk.

Warning: Correlated slashing is the primary threat in restaking. A single validator misbehavior can slash stakes across multiple restaked services simultaneously, potentially wiping out a significant portion of your portfolio in one event.

To manage this exposure, it is essential to monitor the health of the underlying validators and the audit status of the restaking contracts. The risk is not theoretical; historical incidents in DeFi have shown that complex composability often leads to unforeseen failure modes. As the restaking ecosystem matures in 2026, the focus will shift from yield chasing to rigorous risk assessment of the security assumptions embedded in these protocols.

Choosing a restaking strategy for 2026

Selecting a restaking strategy depends on whether you prioritize ETH yield or BTC exposure. The market has split into two distinct paths: ETH-centric protocols like EigenLayer and BTC-focused solutions like Babylon.

If you hold Ethereum, restaking derivatives offer exposure to additional security services without selling your asset. This approach captures yield from both staking and restaking layers. However, it introduces smart contract risk that does not exist in simple staking. Use the live price widget below to track ETH’s current valuation against restaking yields.

For Bitcoin holders, the choice is between native stacking and restaking. Native stacking is simple but yields are fixed by halving cycles. Restaking protocols like Babylon allow you to earn yield while securing other networks. This adds complexity but potentially higher returns. The technical chart below shows recent BTC volatility, which impacts the risk-reward calculation for restaking.

Your decision should hinge on risk tolerance. If you prefer safety, native staking or stacking is preferable. If you seek higher yield, restaking derivatives offer more upside but require active monitoring. Always check the total value locked (TVL) and audit history of any protocol before committing funds.

Restaking derivatives 2026 common: what to check next

Choosing the right platform depends on your risk tolerance and asset preferences. For Bitcoin stacking, Xverse Stacking and LISA are leading options, prioritizing security and non-custodial control. For Ethereum restaking, EigenLayer remains the primary infrastructure, while Babylon introduces new Bitcoin-backed security models.

Market conditions in 2026 require careful timing. Bitcoin’s secular bull trend remains intact, with projections approaching $180,000 despite 2025’s volatility. Restaking yields track these broader market sentiments, offering higher returns but introducing smart contract and slashing risks.

Is 2026 a good year to invest in bitcoin?

Bitcoin enters 2026 with its secular bull market intact, despite what will retrospectively be viewed as an unusually complex and sentiment-disrupting year in 2025. Analysts project it will make new all-time highs and approach $180,000. This optimism supports the broader crypto ecosystem, including restaking derivatives that rely on underlying asset stability.

What is the best platform for stacking?

Top apps for staking and stacking include Xverse Stacking, Acre, LISA, StackingDAO, and Binance. The most important factors for choosing a staking app include fees, security (custodial vs. non-custodial), flexibility, minimum investment, APY rewards, supported assets, convenience, and lock-up periods. For restaking, EigenLayer is the dominant Ethereum platform, while Babylon is emerging for Bitcoin security.

No comments yet. Be the first to share your thoughts!