Restaking derivatives 2026 market context

The restaking narrative has shifted from speculative hype to economic reality. In 2026, the sector is defined by a stark divergence between protocol promises and actual yield generation. Early projections of high passive income have largely evaporated, replaced by a market where restaking serves as a supplementary layer rather than a primary yield engine. The collapse of the "easy money" phase has forced participants to evaluate restaking not as a standalone investment strategy, but as a component of a broader, more complex staking infrastructure.

At the center of this evolution is EigenLayer v2, which aims to standardize the fragmented landscape of Active Verification Services (AVS). The initial rollout saw an excessive proliferation of AVS projects, many of which failed to generate sufficient demand to cover operator costs. This oversupply diluted rewards, pushing incremental yields for restaked ETH below 1%. The market is now consolidating around protocols that can demonstrate genuine utility and sustainable economic models, filtering out the noise of low-value verification tasks.

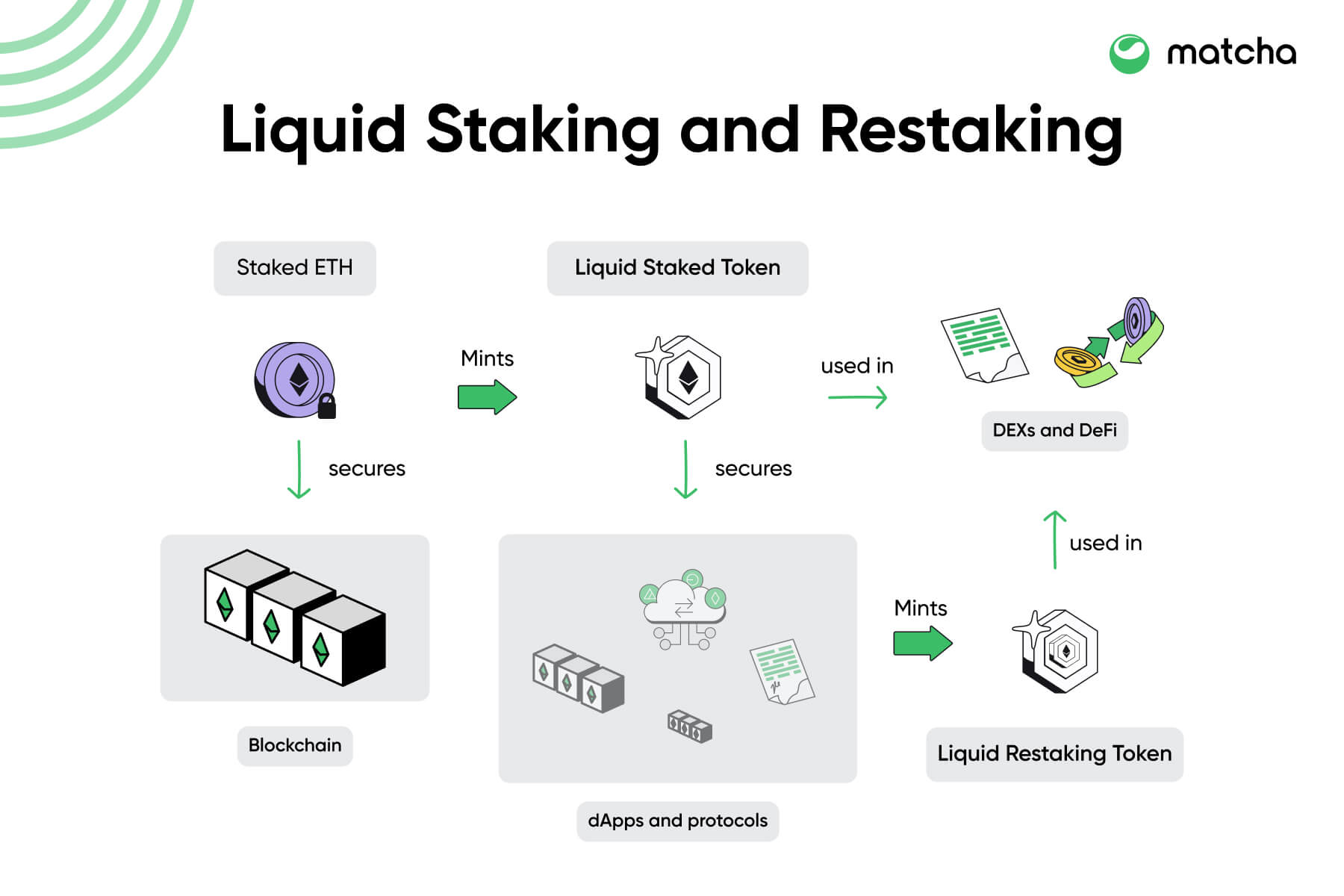

The distinction between solo staking, liquid staking, and restaking has become critical for capital allocation. These models are no longer interchangeable; each serves a specific risk and reward profile. Solo staking offers maximum control and direct protocol rewards, while liquid staking provides liquidity. Restaking, however, introduces additional smart contract and operational risks in exchange for potential, albeit diminished, incremental yields. Investors are increasingly cautious, prioritizing the security of the underlying asset over the marginal gains offered by complex derivative layers.

EigenLayer v2 Protocol Upgrades

EigenLayer v2 represents a structural shift in restaking infrastructure, moving beyond the experimental phase of v1 to address critical scalability and security bottlenecks. The upgrade introduces a more modular architecture for Actively Validated Services (AVS), allowing operators to participate in multiple validation tasks without the linear scaling of computational overhead that plagued earlier iterations. This architectural change is not merely incremental; it fundamentally alters the economic viability of restaking by decoupling validation complexity from security deposit requirements.

The most significant change lies in how AVS selection is managed. In v1, the friction of joining new services often led to centralization, as only the largest operators could afford the integration costs. v2 implements a standardized interface and automated onboarding protocols, reducing the barrier to entry for specialized AVS. This democratization of access encourages a more diverse ecosystem of validators, each contributing unique security guarantees to different layers of the Ethereum stack. The result is a more resilient network where security is distributed across a wider array of independent operators rather than concentrated in a few dominant pools.

Economically, these upgrades aim to stabilize yield volatility by introducing more predictable fee structures and slashing conditions. By clarifying the liability framework for restakers, v2 reduces the uncertainty that often depresses yields during periods of market stress. This stability is crucial for attracting institutional capital, which requires clear risk parameters before committing significant funds to restaking derivatives. The protocol’s evolution signals a maturation of the restaking narrative, shifting focus from raw yield generation to sustainable, long-term security provision.

The integration of these upgrades also impacts the broader liquid restaking token (LRT) ecosystem. LRT protocols must adapt their smart contracts to interface with the new v2 standards, ensuring that yield distribution remains efficient and transparent. This adaptation period may cause temporary fluctuations in yields as protocols recalibrate their strategies, but the long-term outlook points toward more robust and diversified yield sources. As the ecosystem matures, the distinction between traditional staking and restaking will continue to blur, creating a more integrated and efficient capital market for Ethereum validators.

Top liquid restaking tokens compared

Liquid restaking tokens (LRTs) have emerged as the primary derivative layer for EigenLayer v2, allowing stakers to retain liquidity while securing additional protocols. The market has consolidated around a few major protocols that differ significantly in their yield composition, risk profiles, and underlying asset structures. Understanding these distinctions is critical for allocating capital efficiently in a high-stakes environment.

The following comparison highlights the structural differences between the leading LRTs. While all LRTs derive base yield from Ethereum staking, the additional returns come from distinct sources: EigenLayer points, restaking incentives from Actively Validated Services (AVSs), and protocol-specific token emissions.

| Protocol | Underlying Asset | Primary Yield Source | Risk Profile |

|---|---|---|---|

| EigenLayer (eigenLST) | ETH | ETH Staking + AVS Incentives | Medium |

| Puffer Finance | ETH | ETH Staking + Puffer Points | Medium-High |

| Karak Network | ETH | ETH Staking + Karak Points | Medium |

| Renzo Protocol | ETH | ETH Staking + EZ Points | Medium |

Managing Restaking Risk

Restaking amplifies yield potential, but it also layers multiple points of failure onto a single capital deployment. The primary threat is slashing, where a validator operator’s misconduct triggers a penalty that deducts from the staker’s principal. In a restaking context, a single operator failure can slash ETH from EigenLayer and simultaneously trigger penalties across multiple active verification services, compounding the loss beyond what standard solo staking would incur.

Smart contract risk introduces another layer of exposure. Liquid Restaking Tokens (LRTs) rely on complex interoperability between the restaking layer, the LRT wrapper, and individual AVS contracts. A vulnerability in any link of this chain can lead to total loss of funds. Additionally, depegging risk threatens the liquidity of LRTs; if market sentiment turns or the underlying collateral is compromised, the token’s price can decouple from its net asset value, forcing exits at a loss.

Mitigation requires strict due diligence. Stakers should limit exposure to operators with proven track records and transparent slashing insurance mechanisms. Diversifying across multiple AVSs can reduce the impact of a single service failure, while monitoring the health and liquidity of the LRT protocol itself is essential to avoid being trapped during a depeg event. As noted in recent market analysis, the collapse of restaking hype in late 2025 was driven by unsustainable economics and excessive AVS proliferation, highlighting the need for caution in a rapidly evolving landscape [Everstake, 2025].

ETH staking yield outlook for 2026

The yield landscape for Ethereum staking is shifting from passive rewards to active, multi-layered value capture. As EigenLayer v2 matures, the distinction between simple staking and restaking becomes a matter of risk-adjusted return rather than mere yield maximization. Corporate treasuries and institutional participants are increasingly treating restaking not as a speculative gamble, but as a core component of a diversified digital asset strategy. This shift is driven by the need to offset the diminishing returns of base consensus rewards with additional economic activity from restaked protocols.

Current projections suggest that while base ETH staking yields will remain relatively stable, the total value proposition will increasingly depend on the health of the restaking ecosystem. Protocols that offer robust slashing protection and transparent economic incentives are likely to capture the majority of this additional yield. The integration of Liquid Restaking Tokens (LRTs) allows for greater capital efficiency, enabling stakers to participate in multiple security markets simultaneously without locking up their principal. This liquidity is critical for maintaining yield competitiveness in a market where capital mobility is paramount.

Technical analysis of ETH price action remains a secondary but important factor in yield calculations. As the asset's market value fluctuates, the real-world return on investment for stakers changes accordingly. The following widget provides the current market price of ETH, which serves as the baseline for calculating potential annualized percentage yields (APY) across different staking and restaking configurations. Traders and long-term holders alike should monitor these price movements closely, as they directly impact the dollar-denominated returns of staking positions.

Restaking derivatives 2026 FAQ

How does EigenLayer v2 change AVS onboarding compared to v1?

EigenLayer v2 introduces standardized interfaces and automated onboarding protocols for Actively Validated Services (AVS). This reduces the technical friction and integration costs that previously favored large operators, allowing a more diverse set of validators to participate. The result is a more decentralized security model where validation tasks are distributed across a wider network rather than concentrated in a few dominant pools.

What are the primary risks associated with Liquid Restaking Tokens (LRTs) in 2026?

The main risks are correlated slashing and smart contract vulnerability. If an operator misbehaves on any secured AVS, the restaker’s principal can be slashed across multiple layers simultaneously. Additionally, LRTs rely on complex interoperability between the restaking layer, the token wrapper, and AVS contracts; a bug in any link can lead to total loss. Depegging risk also remains, where market sentiment or collateral issues cause the token price to decouple from its net asset value.

Is restaking still profitable in 2026?

Restaking is no longer a source of explosive, speculative yields. The market has corrected from unsustainable APYs to more realistic returns driven by genuine demand for AVS security. Incremental yields for restaked ETH have fallen below 1% in many cases due to oversupply of AVS tasks. Profitability now depends on selecting protocols with robust slashing protection and transparent economic incentives, rather than chasing high nominal rates.

How do institutional players influence the restaking market?

Institutional capital has become a primary liquidity provider, stabilizing rates but reducing the "get rich quick" margins seen in previous cycles. Institutions require clear risk parameters and sustainable economic models, driving the market toward protocols that demonstrate genuine utility and long-term security provision. This shift has forced the consolidation of the restaking landscape, filtering out low-value verification tasks and focusing on protocols that can support large-scale, secure capital deployment.

No comments yet. Be the first to share your thoughts!