How restaking derivatives work in 2026

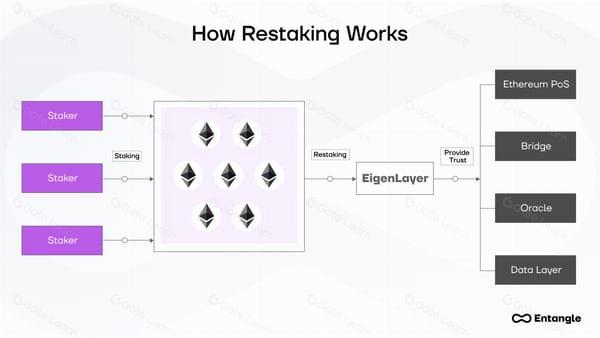

Restaking derivatives, primarily Liquid Restaking Tokens (LRTs), function as a second layer of yield generation built on top of existing liquid staking tokens (LSTs). While standard LSTs like stETH allow holders to trade staked Ethereum, they do not inherently provide additional yield beyond the base Ethereum consensus rewards. LRTs change this dynamic by allowing users to deposit their LSTs into a restaking protocol, effectively reusing the same underlying ETH to secure multiple networks simultaneously.

This mechanism creates a compounding yield structure. The base yield comes from Ethereum’s consensus layer, while the secondary yield is generated by earning rewards for providing security to other protocols, such as oracle networks or bridge validators. Because the same capital is securing multiple services, the total return is the sum of these distinct reward streams. This is not merely a marketing claim; it is a fundamental architectural shift that decouples staking from a single network’s security budget.

The distinction between these models is critical for 2026’s market landscape. Solo staking, liquid staking, and restaking are not interchangeable tools. Solo staking offers maximum control but requires significant technical overhead. Liquid staking provides liquidity at the cost of delegating validator duties. Restaking adds another layer of complexity and potential yield, but it introduces new vectors of risk, including smart contract exposure and the potential for slashing across multiple networks. Understanding this hierarchy is essential for assessing the true risk-adjusted return of any position.

To contextualize the underlying asset performance that drives these yields, we can look at the broader Ethereum market dynamics.

The growth of the restaking sector in 2026 is closely tied to the expansion of the broader staking ecosystem. As more protocols require decentralized security, the demand for reusable staked capital increases. This creates a feedback loop where higher demand for security leads to higher yields, which in turn attracts more capital into the restaking derivatives space. However, this growth is not without its pitfalls, and the complexity of these instruments requires careful navigation.

Comparing Top Liquid Restaking Tokens

Liquid restaking tokens (LRTs) have matured from experimental DeFi primitives into a structured market segment. As of 2026, the landscape is defined by three dominant protocols: Ether.fi, Renzo, and Kelp DAO. Each offers a different balance of yield generation, security delegation, and operational complexity.

The choice between these protocols hinges on how users prefer to manage risk. Ether.fi focuses on native Ethereum security with a diversified validator set. Renzo emphasizes ease of use and broad compatibility with other DeFi protocols. Kelp DAO provides a more modular approach, allowing users to select specific restaking strategies. This section compares their key metrics to help you decide which LRT aligns with your risk tolerance.

Protocol Comparison

The following table summarizes the current state of the leading LRT protocols. Data reflects approximate market conditions and security models as of early 2026.

| Protocol | TVL (Est.) | Base APY | Security Model | User Complexity |

|---|---|---|---|---|

| Ether.fi | $1.2B | 3.5-5.2% | Native ETH + eETH | Medium |

| Renzo | $800M | 4.0-6.0% | EigenLayer + ezETH | Low |

| Kelp DAO | $600M | 3.0-4.8% | Modular (rsETH) | High |

Key Trade-offs

Yield vs. Stability: Renzo often offers higher base APY due to its aggressive restaking strategies, but this comes with higher smart contract risk. Ether.fi provides a more stable yield profile backed by its native eETH token, which is widely accepted across DeFi. Kelp DAO’s rsETH offers flexibility but requires users to understand the underlying restaking layers.

Security Model: Ether.fi’s native Ethereum security is a significant advantage for users concerned about EigenLayer’s newer risk profile. Renzo and Kelp DAO rely heavily on EigenLayer’s restaking infrastructure, which introduces additional layers of smart contract complexity. Users should review the specific slashing conditions for each protocol.

Liquidity and Compatibility: Renzo’s ezETH is designed for seamless integration with other DeFi protocols, making it a popular choice for yield farmers. Ether.fi’s eETH is also widely supported but may have slightly less liquidity in some markets. Kelp DAO’s rsETH is gaining traction but is still building its ecosystem partnerships.

Layering Yield on Restaking Capital

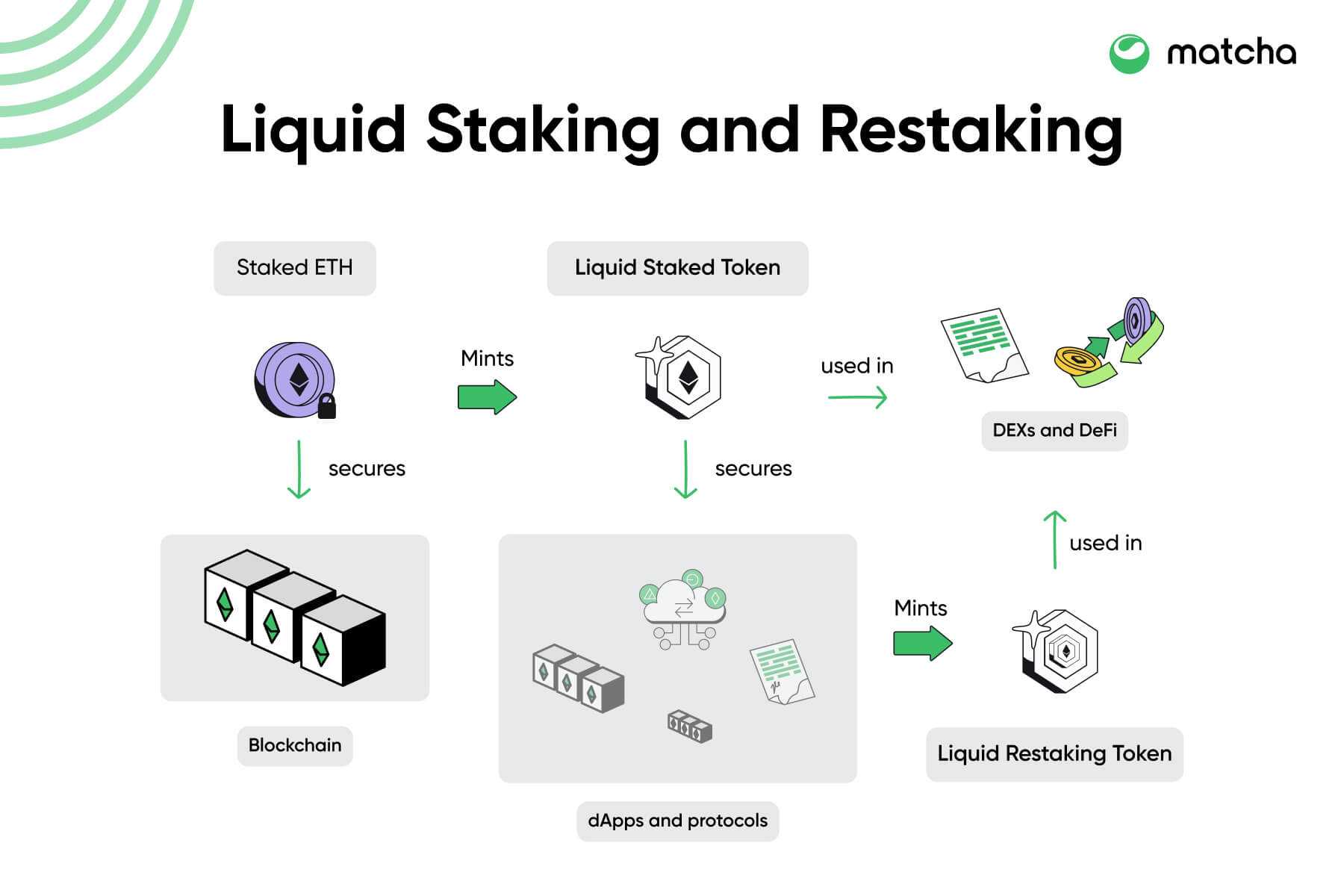

Restaking derivatives (LRTs) are designed to be modular financial instruments rather than static savings accounts. Once capital is secured by EigenLayer or similar protocols, the resulting derivative—such as ezETH or rsETH—enters the broader DeFi ecosystem. This composability allows users to layer additional yield mechanisms on top of the base restaking rewards. The strategy effectively turns a single deposit into a multi-stream income source, though it introduces new vectors for smart contract and liquidation risk.

The most common approach involves supplying the LRT to lending markets like Aave or Morpho. In this setup, the LRT serves as collateral, generating yield from two sources: the base restaking APR and the interest paid by borrowers. Alternatively, users can provide liquidity to decentralized exchange (DEX) pools, such as Uniswap or Balancer. While liquidity mining often offers higher nominal yields, it exposes the position to impermanent loss and requires active management to maintain the desired asset ratio.

To illustrate the relationship between liquid staking and restaking layers, consider the following diagram from Matcha.

Capital efficiency is the primary driver for these strategies. By reusing the same underlying ETH multiple times across different yield-generating protocols, investors can amplify their returns. However, this leverage is not free. Each additional layer of DeFi composability adds complexity and potential points of failure. Users must carefully evaluate the smart contract audits and economic incentives of each protocol they interact with to ensure the additional yield justifies the increased risk exposure.

Regulatory scrutiny and market risks

Liquid restaking tokens (LRTs) operate in a regulatory gray zone that poses significant uncertainty for 2026 strategies. Unlike standard staking, LRTs involve complex layers of delegation and yield optimization that regulators may classify as securities. This classification could trigger strict compliance requirements, potentially limiting liquidity or imposing heavy reporting burdens on protocols and users alike.

Legal experts warn that the multi-protocol nature of restaking amplifies these risks. When assets are restaked across multiple networks, the resulting tokens may fail howey test exemptions due to the expectation of profit from the efforts of others. The lack of clear precedent means that enforcement actions could emerge unexpectedly, disrupting market access for LRT providers.

Beyond regulatory hurdles, technical slashing risks remain a critical concern. Restaking increases the attack surface for validators, as a single slashing event can impact multiple protocols simultaneously. This compounding risk means that potential losses are not just theoretical but can result in significant capital erosion during network failures or malicious attacks.

The intersection of regulatory ambiguity and technical vulnerability creates a high-stakes environment. Investors must carefully assess the legal standing of each protocol and understand the slashing conditions before committing capital. As the market matures, clarity is expected to emerge, but for now, the risks remain substantial and largely unmitigated by insurance or regulatory safeguards.

Frequently asked questions about restaking

Restaking derivatives and liquid staking represent the current yield frontier, but they operate in a distinct regulatory and technical landscape compared to traditional crypto investments. Below are direct answers to common questions regarding ETF exposure and network mechanics.

No comments yet. Be the first to share your thoughts!