Defining restaking derivatives 2026

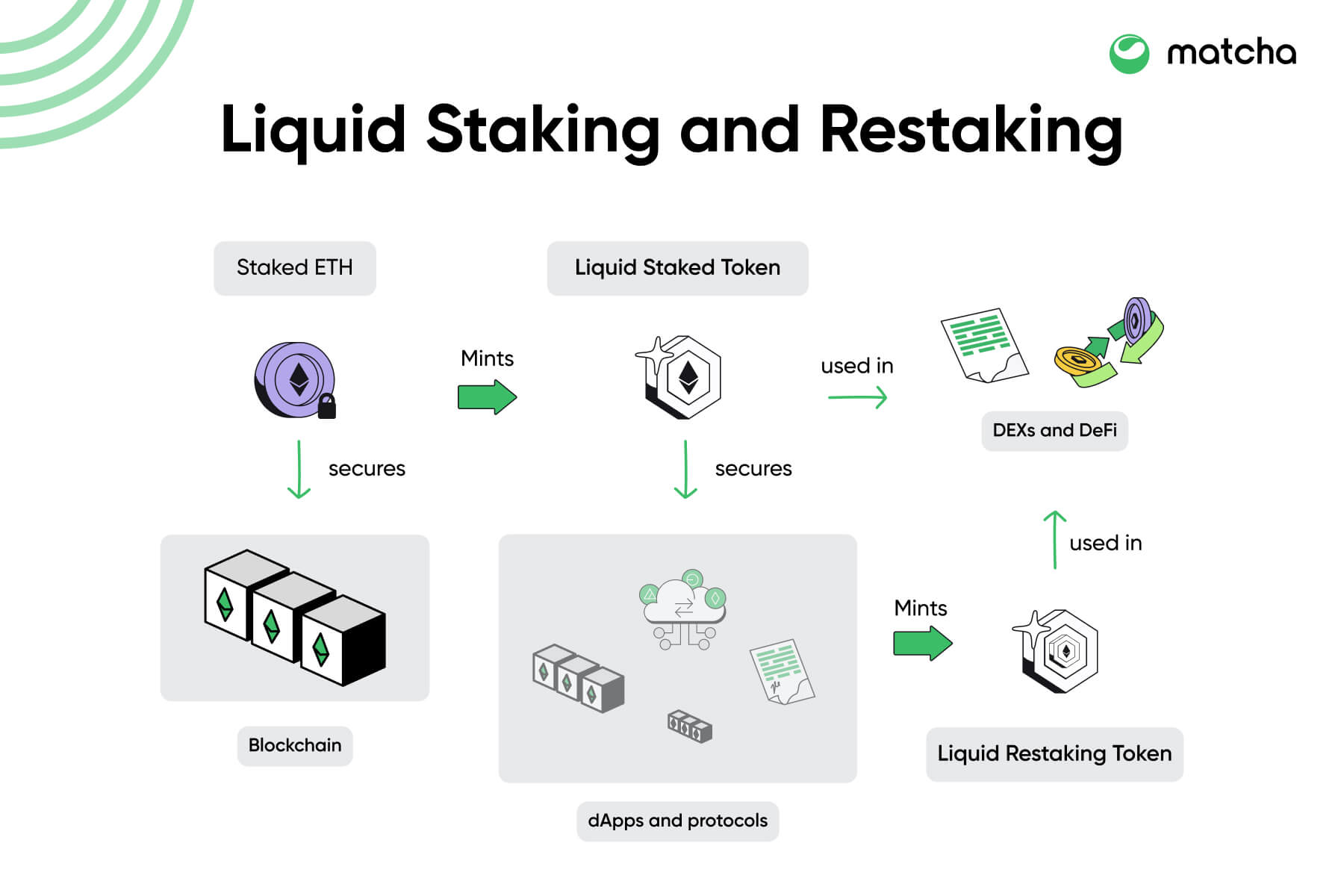

Restaking derivatives, or Liquid Restaking Tokens (LRTs), represent a structural evolution of standard liquid staking. While a Liquid Staking Token (LST) like stETH simply represents a claim on staked ETH and its base yield, an LRT introduces a secondary layer of delegation. This mechanism allows validators to reuse their already-staked ETH to secure additional protocols, effectively creating a new asset class that decouples security from the base Ethereum layer.

The technical foundation of this model relies on the concept of "shared security." In a standard staking setup, a validator’s ETH secures only the Ethereum consensus layer. In restaking, that same ETH is locked in a smart contract—such as EigenLayer—that acts as a middleware layer. This contract then distributes the validator’s security to "restaking services," which can be anything from oracle networks to bridge validators. The holder of an LRT receives yield from both the base Ethereum staking rewards and the additional incentives provided by these secondary protocols.

This architecture creates a complex risk profile that differs significantly from traditional staking. The primary risk is "shared slashing." If a validator misbehaves while providing security to a secondary protocol, the penalty applies to the entire staked amount, not just a portion allocated to a specific task. Consequently, LRTs are not merely yield-bearing instruments; they are financial instruments that bundle protocol risk with cryptographic security. Understanding this distinction is critical for evaluating the true cost of capital in the 2026 DeFi landscape.

To visualize the underlying asset performance, we track the primary benchmark for this sector. The chart below reflects the broader market movement of the underlying asset, which drives the base yield component of all LRTs.

Restaking market growth and capital flows

The restaking ecosystem is expanding rapidly as capital seeks yield in modular security. Market research projects the sector will grow from USD 21.8 billion in 2026 to USD 198.7 billion by 2034, reflecting a compound annual growth rate of 31.2% Intel Market Research. This trajectory signals a structural shift rather than a speculative spike, as institutional participants increasingly view restaking as a core infrastructure layer.

Capital is flowing into Liquid Restaking Tokens (LRTs) not just for yield, but for the composability they offer. As noted in 2026 industry analysis, corporate treasuries and DeFi protocols are integrating restaking networks to maximize capital efficiency while maintaining security guarantees DAIC Capital. This dual demand drives the volume, linking restaking activity directly to the performance of the underlying asset.

To contextualize this growth, the value of restaking derivatives is closely tied to the price action of Ethereum. The chart below illustrates ETH/USD performance, which serves as the primary collateral base for most restaking protocols.

Comparing top LRT protocols

Liquid restaking tokens (LRTs) have evolved from experimental yield strategies into distinct financial products with varying risk profiles. While the core mechanism—locking staked assets to secure multiple networks—remains consistent, the execution differs significantly across protocols. Understanding these differences is essential for capital allocation in 2026.

The primary divergence lies in yield sourcing and security architecture. Some protocols rely heavily on Ethereum's native staking yield plus restaking rewards, while others integrate Bitcoin restaking or cross-chain liquidity. Security models also vary, with some using single-validator setups and others employing decentralized validator networks to mitigate slashing risks.

The following comparison highlights key structural differences between leading LRT protocols. Data reflects current protocol configurations as of early 2026.

| Protocol | Primary Yield Source | Security Model | Supported Chains | Key Risk Factor |

|---|---|---|---|---|

| EigenLayer | ETH staking + restaking rewards | Single-asset restaking (ETH) | Ethereum | Smart contract complexity |

| Ether.fi | ETH staking + LRT derivatives | Multi-asset restaking | Ethereum, Arbitrum, Base | Liquidity fragmentation |

| Puffer Finance | ETH staking + insurance pool | Slashing insurance + decentralized validators | Ethereum | Insurance pool solvency |

| Babylon | BTC staking + security sharing | Time-lock based security | Bitcoin, Ethereum | Cross-chain bridge risk |

Yield mechanics and risk choices that change the plan

Liquid Restaking Tokens (LRTs) generate yield through a layered structure. Validators stake ETH on Ethereum, earning the base protocol reward. They then delegate that staked ETH to restaking protocols like EigenLayer, which secure additional "Actively Validated Services" (AVSs). In return, validators earn extra fees from these services. The LRT protocol aggregates these multiple income streams and issues a liquid token representing the position. Holders benefit from the compounded yield without managing validator infrastructure.

This structure introduces specific risks that differ from standard staking. The primary concern is slashing. If a validator behaves maliciously or goes offline, Ethereum penalizes the stake. Because LRT positions are often shared across many protocols, a single slashing event can drain funds allocated to multiple AVSs simultaneously. This creates a "contagion" risk where one protocol failure impacts the entire restaked balance.

Smart contract vulnerability is the second major risk vector. LRTs require complex code to manage withdrawals, reward distribution, and delegation. Each additional layer of code increases the attack surface. A bug in the LRT contract or the underlying restaking protocol can lead to total loss of funds. Unlike native staking, where the risk is limited to validator performance, LRTs expose users to the technical reliability of multiple independent codebases.

Users must weigh the higher APY against these compounded risks. The yield premium is not guaranteed; it depends on the demand for AVS security and the continued integrity of the smart contracts. For conservative investors, the complexity of managing multi-layered risk may outweigh the marginal gain in yield.

Key Questions on Restaking Safety

Investors navigating restaking derivatives in 2026 must distinguish between solo staking, liquid staking, and restaking models, as these mechanisms are not interchangeable [1]. Understanding the specific risk profile of each layer is essential for capital preservation.

Are restaking derivatives safe?

Restaking introduces multiplicative risk. While it amplifies yield, it also exposes staked assets to multiple smart contract vulnerabilities simultaneously. A failure in a single restaking protocol can trigger cascading liquidations across dependent services. Investors should treat these yields as compensation for systemic risk, not guaranteed income.

What is the regulatory outlook for LRTs?

Regulatory clarity remains fragmented. As of 2026, no major jurisdiction has fully classified Liquid Restaking Tokens (LRTs) as either securities or commodities. This ambiguity creates compliance risks for institutional participants. Projects operating without clear legal frameworks may face sudden restrictions or delistings.

Is the yield sustainable?

Current yields often rely on inflationary emissions or subsidies from restaking protocols. Historical data shows that once subsidies decrease, yields compress significantly. Investors should analyze the underlying value accrual mechanisms rather than relying on short-term APY figures.

No comments yet. Be the first to share your thoughts!