Defining restaking derivatives in 2026

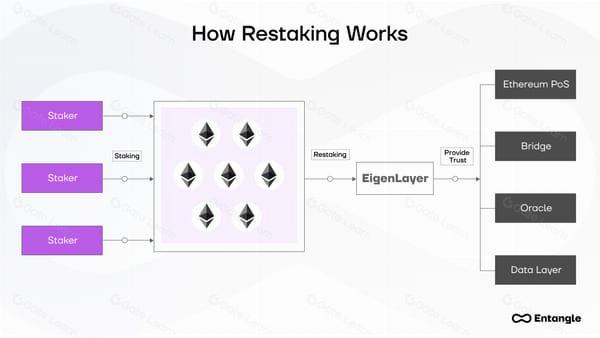

Restaking derivatives, often called Liquid Restaking Tokens (LRTs), represent a structural evolution in how Ethereum validators utilize their staked capital. While traditional Liquid Staking Tokens (LSTs) like stETH allow users to maintain liquidity while earning base validator rewards, LRTs take that already-tokenized stake and restake it to secure additional decentralized services. This creates a nested hierarchy of trust where a single unit of ETH contributes to the security of Ethereum itself and secondary networks simultaneously.

The distinction is not merely semantic; it is a fundamental shift in capital efficiency. In a standard LST model, the staked ETH is locked in the Ethereum consensus layer. In a restaking model, that same ETH is re-delegated to act as economic security for oracles, bridges, and other middleware protocols. This double-counting of security is the core value proposition but also the primary source of systemic risk. The capital is no longer passive; it is actively engaged in a multi-layered verification process.

As the ecosystem matures in 2026, the regulatory and technical complexity of these instruments has intensified. Understanding the mechanics is essential before evaluating yield strategies. The underlying asset remains Ethereum, but the derivative’s risk profile is significantly more complex than simple staking.

Regulatory scrutiny facing liquid restaking

The classification of Liquid Restaking Tokens (LRTs) remains the single most significant legal hurdle for institutional adoption in 2026. Regulators in the United States and the European Union are increasingly viewing restaked assets through the lens of the Howey Test, raising the question of whether these tokens constitute unregistered securities.

In the United States, the Securities and Exchange Commission (SEC) has maintained a cautious stance, often treating staking derivatives as securities when they offer yield expectations tied to network validation efforts. This ambiguity creates a compliance minefield for institutions. Unlike direct staking, where the validator relationship is direct, LRTs introduce an intermediary layer. This layer obscures the underlying asset's legal status, making it difficult to determine if the token is a commodity or a security. The lack of clear guidance forces many institutions to avoid LRTs entirely, limiting market liquidity and depth.

The European Union’s Markets in Crypto-Assets (MiCA) regulation offers a different framework. While MiCA provides a clearer regulatory path for asset-referenced tokens and e-money tokens, its treatment of staking derivatives is still evolving. The regulation focuses heavily on transparency and reserve requirements, but it does not explicitly exempt restaking mechanisms. This means that even in a regulated environment, LRT issuers must navigate complex compliance landscapes regarding custody and risk disclosure. The absence of a "safe harbor" for restaking protocols means that legal risks persist regardless of the jurisdiction.

For institutional participants, this regulatory uncertainty translates into higher operational costs and slower deployment. Legal teams must conduct rigorous due diligence on each LRT protocol to assess its security status. This process is costly and time-consuming, often outweighing the yield benefits of restaking. As a result, institutional capital remains largely sidelined, with only the most legally sophisticated players entering the space. The market is currently in a holding pattern, waiting for clear regulatory precedents to emerge.

The long-term viability of LRTs depends on how protocols adapt to these regulatory pressures. Some issuers are exploring "permissioned" restaking models that restrict participation to accredited investors, effectively creating a private securities market. While this approach mitigates regulatory risk, it fundamentally contradicts the open-access ethos of DeFi. Other protocols are seeking formal legal opinions to clarify their status, but these opinions are not binding on regulators. Until a definitive regulatory framework is established, LRTs will remain a high-risk asset class for institutional portfolios.

Comparing top restaking protocols and yields

The restaking landscape has fragmented into distinct ecosystems, primarily dividing between Ethereum-native infrastructure and Solana-based yield aggregators. Understanding these structural differences is essential for assessing both yield potential and regulatory exposure. EigenLayer remains the dominant force in Ethereum restaking by total value locked (TVL), leveraging its Actively Validated Services (AVS) model to distribute risk across a wide array of decentralized infrastructure tasks. In contrast, Jito dominates the Solana restaking market by capturing MEV (Maximal Extractable Value) alongside standard staking rewards, offering a different risk-reward profile tied to Solana's transaction throughput.

YieldNest represents a newer entrant focused on liquid restaking tokens on Ethereum. By abstracting the complexity of managing multiple AVS delegations, YieldNest aims to provide a more streamlined yield vehicle, though its TVL remains significantly smaller than the incumbents. This fragmentation means that yield metrics are not directly comparable without accounting for the underlying asset risk and the specific revenue sources—whether from consensus rewards, MEV, or protocol fees.

The following comparison outlines the key operational differences and risk factors for the leading protocols. Data reflects market conditions as of early 2026.

| Protocol | Primary Chain | TVL Scale | Primary Yield Source | Jurisdictional Note |

|---|---|---|---|---|

| EigenLayer | Ethereum | Large | AVS Fees + Staking Rewards | US-based; SEC scrutiny on DeFi intermediaries |

| Jito | Solana | Large | MEV + Staking Rewards | US-based; MEV classification under debate |

| YieldNest | Ethereum | Emerging | LRT Yield + AVS Fees | US-based; LRT tokenization risks |

| Ether.fi | Ethereum | Large | ETH Staking + Restaking Fees | US-based; DAO structure considerations |

| Renzo | Ethereum | Medium | Restaking + Strategy Fees | US-based; Automated strategy risks |

When evaluating these options, investors must distinguish between passive staking yields and active restaking yields. EigenLayer and Ether.fi require users to actively manage or delegate their restaking exposure to specific AVSs, which introduces smart contract and slashing risks. Jito’s model is more automated but exposes users to Solana-specific network risks and MEV volatility. YieldNest and Renzo attempt to mitigate complexity through automated strategy management, but this centralization of logic can create a single point of failure.

The regulatory environment remains the primary variable. In the United States, the SEC has not issued explicit guidance on restaking tokens, but its enforcement actions against DeFi platforms suggest that any protocol acting as an unregistered securities exchange or investment contract facilitator faces significant legal risk. Protocols with clear US-based operational teams, like EigenLayer and Jito, are subject to heightened scrutiny. Conversely, protocols with distributed governance or offshore operational hubs may face different legal challenges, though the US extraterritorial reach often applies.

For high-stakes capital allocation, the choice often comes down to risk tolerance. Conservative investors may prefer established Ethereum LSTs like Lido or Rocket Pool, which have lower yield but also lower smart contract risk. Aggressive yield seekers may look to Jito for its MEV upside or EigenLayer for its AVS diversity, accepting the higher complexity and potential for slashing events. Always verify the current TVL and yield metrics, as these can shift rapidly with market conditions and protocol upgrades.

Managing risk in layered yield strategies

Restaking introduces a compounding layer of risk that traditional staking does not face. While solo staking isolates validators to a single consensus layer, restaking protocols like EigenLayer allow operators to pledge their Ethereum (ETH) security to multiple Actively Validated Services (AVS) simultaneously. This composability multiplies potential yield but also creates a single point of failure: if an operator violates the rules of any one AVS, the penalty—slashing—applies to the entire staked position. The underlying ETH is not just locked; it is leveraged across multiple protocols, meaning a failure in one layer can drain capital intended for others.

The primary risk vectors are smart contract vulnerabilities and slashing conditions. Smart contract risk arises because restaking involves complex interactions between liquid staking tokens (LSTs), restaking protocols, and the AVS itself. A bug in any one of these contracts can lead to loss of funds. Slashing risk is more severe. If an operator is proven to have acted maliciously or negligently in an AVS, the Ethereum consensus layer can slash the staked ETH as a penalty. This penalty is not limited to the portion of stake allocated to that specific AVS; it often affects the total restaked balance, effectively confiscating the capital secured across all linked services.

To mitigate these risks, investors must prioritize protocol selection and operator due diligence. Rather than chasing the highest yield, which often correlates with higher risk or less mature AVSs, focus on protocols with extensive audit histories and clear, enforceable slashing conditions. Additionally, diversifying across multiple LST providers and AVSs can reduce exposure to any single point of failure. However, true diversification is difficult in restaking because the underlying collateral (ETH) remains shared. The most effective strategy is to view restaking not as a passive income stream, but as an active security provision service that requires ongoing monitoring of operator performance and protocol updates.

Key questions on restaking compliance

Restaking derivatives operate in a complex regulatory environment where legal clarity often lags behind innovation. While Ethereum successfully transitioned from proof-of-work to proof-of-stake in September 2022, the specific classification of Liquid Restaking Tokens (LRTs) remains ambiguous across major jurisdictions. This uncertainty creates distinct risks for institutional and retail participants alike.

Is Ethereum mining still relevant?

No. Ethereum mining ended permanently in 2022 with the Merge. Modern restaking strategies rely entirely on staked Ether rather than computational hashing power. This shift eliminates energy-intensive validation, making staking a more capital-efficient mechanism for securing the network and earning yields through protocol fees and consensus rewards.

How do regulators view LRTs?

Regulatory scrutiny is intensifying as LRTs allow users to stake Ether on multiple protocols simultaneously. Legal analyses suggest that if these tokens are deemed securities, they may fall under strict jurisdictional oversight. Investors should consult official sources and legal opinions specific to their region, as enforcement priorities vary significantly between the United States, the European Union, and other markets.

What are the primary risks of restaking?

The core risk lies in the amplification of exposure. By restaking, you are securing multiple networks with the same collateral. If one protocol fails or suffers a slashing event, your entire staked position could be penalized. Unlike traditional staking, where risks are isolated, restaking concentrates systemic risk, requiring rigorous due diligence on the underlying protocols and their smart contract security.

No comments yet. Be the first to share your thoughts!