Restaking derivatives 2026 market overview

Liquid Restaking Tokens (LRTs) have shifted from experimental protocols to a foundational layer of decentralized finance. In 2026, the distinction between solo staking, liquid staking, and restaking is no longer a matter of preference but of structural necessity. These models serve different risk profiles and yield expectations, and treating them as interchangeable leads to significant exposure to smart contract and slashing risks.

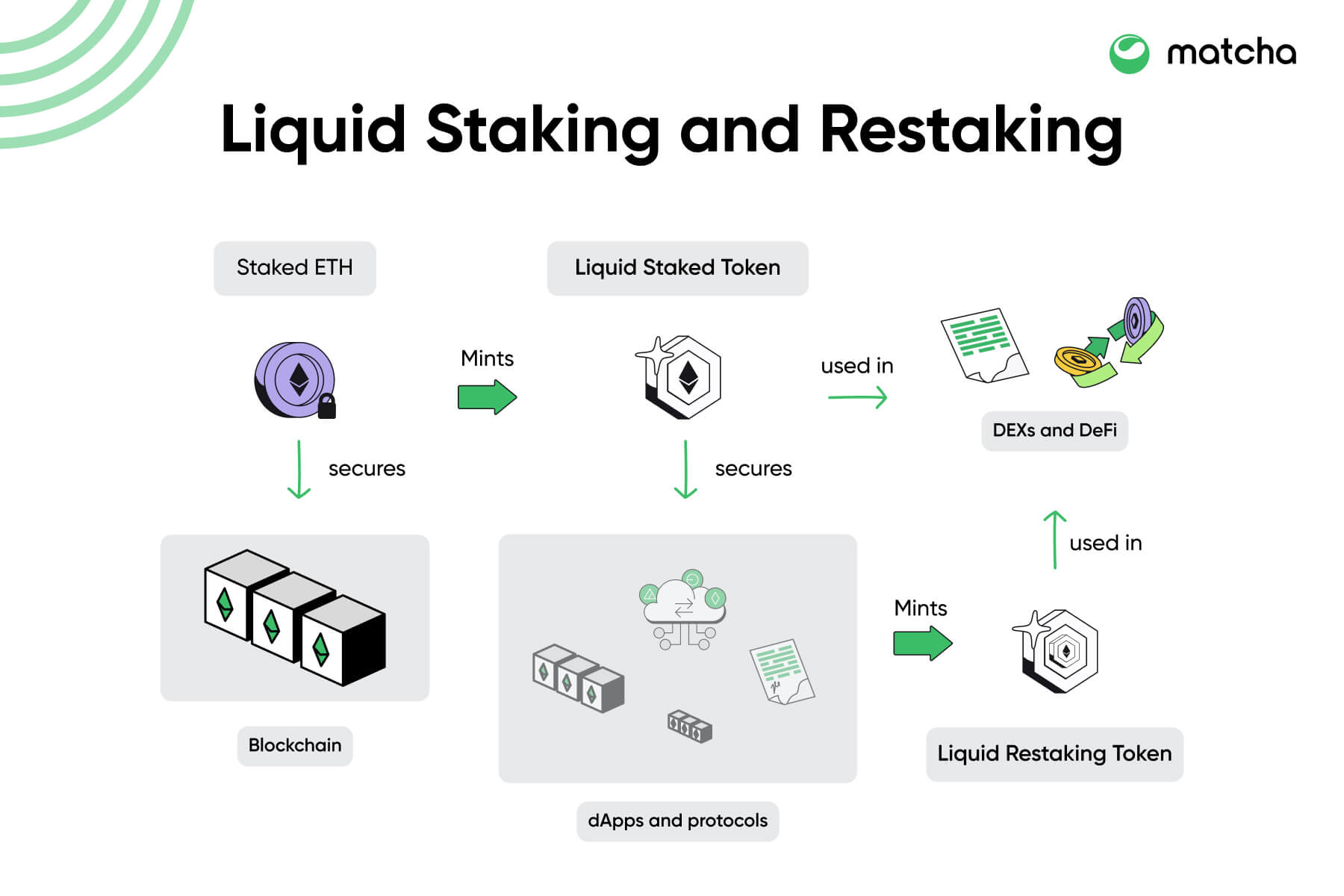

The market has matured beyond the initial "yield farming" phase. Capital that was previously trapped in static staking positions is now being deployed across multiple layers of security services. This transformation allows staked assets to generate multi-layer yield through Active Validation Services (AVSs), effectively turning single-purpose validators into multi-purpose infrastructure providers.

Yield comparisons in this environment require precise data rather than vague descriptors. Current returns are driven by a combination of base Ethereum staking rewards, restaking incentives from EigenLayer, and additional yield from specific AVS integrations. Understanding these mechanics is essential for evaluating risk-adjusted returns in a high-stakes financial landscape.

Comparing top liquid restaking protocols

Liquid restaking tokens have evolved from simple yield aggregators into complex financial instruments with distinct risk profiles. While EtherFi and Renzo established early market dominance through robust validator infrastructure, newer entrants like Puffer and YieldNest are introducing structural innovations to address capital efficiency and security fragmentation.

The primary differentiator among leading protocols is not merely the nominal APR, but the composition of that yield and the underlying security model. EtherFi relies heavily on its native eETH derivative and EigenLayer AVS exposure, while Renzo distributes yield across a broader set of staked assets. Puffer introduces insurance mechanisms via its PufferVault, and YieldNest focuses on simplified, non-custodial yield optimization with lower complexity.

To facilitate a direct comparison, the table below outlines key metrics including base APR estimates, primary AVS exposure, and withdrawal flexibility for the top four LRT protocols as of 2026.

| Protocol | Est. Base APR | Primary AVS Exposure | Withdrawal Flex |

|---|---|---|---|

| EtherFi | 3.5-5.2% | EigenLayer | Instant via eETH |

| Renzo | 3.2-4.8% | EigenLayer + Restake | Instant via ezETH |

| Puffer | 4.0-6.1% | EigenLayer + PufferVault | Variable (Insurance-backed) |

| YieldNest | 3.8-5.5% | EigenLayer | Instant via ynETH |

Yield composition varies significantly across these platforms. EtherFi and Renzo derive a substantial portion of their returns from EigenLayer restaking fees, which are subject to AVS performance and slashing risks. Puffer’s higher estimated APR often reflects the inclusion of insurance premiums and more aggressive AVS selection, which introduces additional smart contract risk. YieldNest attempts to balance yield with simplicity by limiting its AVS portfolio, potentially offering more stable, albeit slightly lower, returns.

Withdrawal flexibility remains a critical operational consideration. Most LRTs offer instant liquidity through their native derivatives (eETH, ezETH, ynETH), but Puffer’s insurance-backed model may impose variable withdrawal conditions depending on vault health. Investors should prioritize protocols with transparent, audited smart contracts and clear slashing risk disclosures over those promising the highest nominal yields.

Decoding restaking risks and rewards

Restaking introduces a leverage multiplier to capital efficiency, but it fundamentally alters the risk profile of staked assets. When you restake, you are not merely earning yield; you are extending the security guarantees of your validator to additional protocols. This creates a reward multiplier effect, as the same ETH can generate yield from Ethereum consensus layers and multiple restaking protocols simultaneously.

However, this efficiency comes with concentrated risk vectors that do not exist in standard staking. The primary concern is slashing. In a restaking environment, a single validator misbehavior can trigger penalties across all attached protocols. If a validator signs conflicting blocks or goes offline, the slashing event deducts from the total staked amount, affecting every protocol relying on that security.

Beyond slashing, smart contract risk is amplified. Restaking protocols sit between the Ethereum consensus layer and application protocols. A vulnerability in any layer of this stack can lead to total loss of the underlying asset. Unlike traditional staking, where the risk is isolated to the validator operator, restaking exposes capital to the code of multiple dependent protocols.

Liquidity risk also plays a critical role. While LRTs provide liquidity, the value of these tokens is derived from the underlying staked ETH and the yield it generates. If the yield expectations shift or if slashing events occur, the token price can decouple from ETH, creating volatility for holders who may need to exit positions quickly.

The reward multiplier is real, but it is not free. You are trading diversification of risk for concentration of exposure. Understanding the specific slashing conditions and smart contract audits of each protocol is essential before committing capital.

Regulatory scrutiny and compliance shifts

The regulatory environment for liquid restaking tokens is tightening as 2026 progresses. While restaking offers higher yields by reusing staked ETH across multiple protocols, it simultaneously concentrates risk. Regulators are increasingly viewing these instruments through the lens of existing securities and commodities frameworks, focusing on how tokens are marketed and how user funds are custodied.

Compliance requirements are forcing protocol designers to rethink their architecture. The primary concern is the legal classification of the derivative token itself. If an LRT is deemed a security, the issuing protocol must register with relevant authorities or find an exemption. This has led to a divergence in protocol design: some platforms are moving toward permissioned staking pools to ensure only qualified investors participate, while others are attempting to structure their tokens as pure utility instruments to avoid securities laws.

User custody is another critical area of scrutiny. Traditional staking involves locking funds in a smart contract with a validator. Restaking adds a layer of complexity where those same funds are used to secure other networks. If a downstream protocol fails, the restaked assets are at risk. Regulators are asking who is liable in such scenarios: the LRT provider, the validator, or the downstream protocol. This ambiguity is driving a push for more transparent risk disclosures and clearer legal frameworks for liability.

The impact on yield is also significant. As compliance costs rise, protocols may need to allocate a portion of their yield to legal and regulatory reserves. This could compress the risk-adjusted returns that attract users in the first place. Investors must now evaluate not just the APY, but the regulatory resilience of the protocol offering that yield. A high-yield instrument may be offering a premium for unaddressed regulatory risk.

Choosing the right restaking strategy

Selecting a restaking protocol requires aligning your risk tolerance with your yield expectations. The landscape has bifurcated into passive yield accumulation and active participation in Actively Validated Services (AVSs). Understanding this distinction is the first step in avoiding structural risks that often accompany higher yields.

Passive Yield: Liquid Restaking Tokens

For investors seeking exposure to restaking yields without managing operational complexity, LRTs offer a streamlined entry point. Protocols like EtherFi or Renzo allow you to stake ETH or LSTs and receive a derivative token that accrues restaking rewards. This approach simplifies the process but introduces smart contract risk from both the underlying LST and the restaking layer.

Active Yield: Direct AVS Participation

Direct participation involves delegating staked assets to specific AVSs. This strategy allows for targeted yield optimization but requires active monitoring of slashing conditions and protocol health. The yield potential is often higher, but the risk of slashing—losing principal due to validator misbehavior—increases significantly. This path is suitable for those willing to engage deeply with protocol documentation and risk parameters.

Comparing Risk-Adjusted Returns

The choice between passive and active strategies hinges on your ability to manage operational risk. Passive LRTs provide diversification across multiple AVSs, reducing single-point failure risks. Active participation offers transparency and potentially higher yields but demands rigorous due diligence. Evaluate each protocol’s slashing history and insurance mechanisms before committing capital.

Common questions about restaking

Restaking derivatives allow users to earn rewards on staked crypto while preserving liquidity and improving capital efficiency. However, the mechanics introduce distinct risks that differ from standard staking.

No comments yet. Be the first to share your thoughts!